The System of Environmental Economic Accounting (SEEA)[1] is the accepted international standard for environmental-economic accounting, providing a framework for statistics on the environment and its relationship with the economy.

In March 2021 the United Nations Statistical Commission adopted the SEEA Ecosystem Accounting (SEEA EA) as a new international statistical standard to integrate ecosystems and their services into national accounting, and to account for biodiversity and ecosystems in national economic planning and policy decision-making.

It brings together economic and environmental information in an internationally agreed set of standard concepts, definitions, classifications, accounting rules and tables to produce internationally comparable statistics. The adoption of the SEEA framework by the United Nations was a major milestone for the statistical community and beyond. The system is, by design, reliant on earth observation to systematically assess the health and status of ecosystems and the benefit of ecosystem flows to human well-being and the economy.

This article intends to bring awareness on this emerging international concept and introduce the opportunities for the EO community.

- The SEEA Framework

The SEEA was developed in two steps. In 2012, the SEEA Central Framework was adopted by the United Nations Commission, and it was then extended and accepted as a statistical standard in 2021. The Central Framework measures economic activities of governments, households, businesses and looks at how much is spent for protecting the environment and examines at exchanges of some of these environmental related products (energy, water…) between the different economic units. It enables to measure the spin overs and the trade-offs and report on stocks and flows of natural capital. It also measures the individual assets within the environment (e.g., in a wetland ecosystem we can account for things like the stock and quality of the water, and the richness of the species present, this gives us a clear description of the asset – or natural capital, other assets are those related to mineral energy resources, timber etc).

The Central Framework constitutes a paradigm shift in the appreciation and valuation of natural resources as the economy sits within the environment component. In other words, the economy must consider the environment as the measurements of activities and economic instruments are related to the environment. On that account, SEEA brings together environmental accounting and economic information to produce internationally comparable statistics.

Ecosystem accounting takes a special approach as it measures the functioning of the ecosystem as an integrated entity and relationships between the biotic and its components within an ecosystem and it is focused on a specific area such as a country, an administrative region, a river basin, etc. It identifies ecosystem units (in which each ecosystem is contiguous) and presents the typology of ecosystems to measure in a consistent way the ecosystem types.

If we take the example of forestry, ecosystem accounting measures the extent of the ecosystem, the conditions (quality of the ecosystem, such as the soil depth), the ecosystem services (biomass of forests filters water and cleans it…), and the contribution of the ecosystem to the economy and benefits (cleaner water being used by beneficiaries such as households or businesses…). Organizing this information can help decision-makers understand how the environment interacts with the economy.

- Policy context

The overall policy context demonstrates a serious effort in the European Union (EU) to have ecosystem accounting becoming part of the standard of environmental information datasets that policy makers will consider.

First, the European Union’s Green Deal[2] covers many environmental dimensions and address transformations of the economy’s components and consumers’ behaviours (example: Farm to Fork strategy[3]). At the core of the Green Deal is the acknowledgment of the interconnections between the environment and economy. Therefore, SEEA Central Framework helps to make more informed decisions across a range of sectors and is key measuring progress to reach these objectives.

The European Commission adopted the New EU Forest Strategy for 2030[4], a flagship initiative of the European Green Deal that builds on the EU Biodiversity Strategy for 2030. As forest management is the main source of biomass for energy and wood production, more robust accounting rules and governance for forest management will provide a solid basis for Europe's future renewables policy in the context of the 2030 climate and energy framework. This is particularly relevant in the context of the Land use and Forestry Regulation (LULUCF)[5] where the Council and Parliament agreed on various pieces of legislation which set the framework for how emissions from the LULUCF sector will be measured and monitored and the role they will play in meeting the EU’s 2030 targets with the objective to decrease gas emissions and increase removals in the land and forestry sector.

Finally, the statistical office of the European Union, EUROSTAT is currently working at anchoring ecosystem accounting at the EU level by developing a proposal for a module for ecosystem accounting to be including in EU environmental accounts (to be adopted), which is a statistical obligation under the members states responsibility.

- The next steps and challenges ahead

The development and the implementation of Ecosystem Accounting will present many opportunities and challenges. At the UN level, the next challenge will be to promote the implementation of the standard with 89 countries implementing the SEEA Central Framework, 34 countries compiling SEEA Ecosystem Accounts and 27 countries planning to start implementing the SEEA.

At EU level and over the past few years, Eurostat, the United Nations, statistical offices and the research community have been working together to provide and overview on ecosystem accounts at EU-level in the (INCA) project. This project has been a model on how Ecosystem accounts addresses key European policy objectives such a as the EU Biodiversity Strategy. All this information can be useful for other policies that have an impact on natural capital, such as agriculture or transport allowing for monitoring the status of ecosystem assets over time and thus give an indication of the change of their status.

At EARSC, we have organized a first EOcafe[6] to respond to the question on how geospatial data and Earth Observation can contribute to ecosystem accounting. EO is widely recognized as a major source of information to monitor the extent, condition and services of their ecosystems. Therefore, for the EO community, it is interesting to note that EO datasets constitute an important source in the construction of ecosystem accounting and can support their implementation by tracking changes in the extent and the condition of ecosystems or measuring ecosystem services. Ecosystem accounts are inherently spatial accounts, with the implication that they strongly depend on the availability of spatially explicit datasets, including Earth Observations. The emergence of dense EO data streams at appropriate scale combined with the advances in digital technologies offer unprecedented opportunities for countries to efficiently monitor the extent and conditions of their ecosystems determine ecosystems services and implement their ecosystem accounting.

Many opportunities will arise to use global databases and Earth Observation to try to compile stage 1 ecosystem account for all countries and the objective is to nationalize these ecosystem accounts and improve them with national datasets and implement them at the national level.

The international Research & Innovation platform ARtificial Intelligence for Environment and Sustainability (ARIES for SEEA[7]) is an Artificial Intellligence Tool using global models, with the objective to support the compilation of some Central Framework accounts. ARIES for SEEA provides initial functionality for assessing ecosystem extent, condition (including pilot set of accounts for forests, which can be easily expanded to other ecosystems and condition variables), and physical accounts for selected ecosystem services using earth observation combined with the appropriate biophysical models.

There is little doubt that the Ecosystem Accounting will provide many opportunities for the EO sector to contribute to the objectives of the Green Deal. ESA plans to issue a first call on Earth Observation for ecosystem accounting, as part of a broad activity called “Pioneer – EO science for society”.

[1] Framework that integrates economic and environmental data to provide a more comprehensive and multipurpose view of the interrelationships between the economy and the environment and the stocks and changes in stocks of environmental assets, as they bring benefits to humanity. More athttps://seea.un.org/ and https://seea.un.org/ecosystem-accounting

[2] The European Green Deal is a set of policy initiatives by the European Commission with the overarching aim of making the European Union (EU) climate neutral in 2050. More information https://ec.europa.eu/clima/eu-action/european-green-deal_en

[3] aiming to make food systems fair, healthy and environmentally-friendly. More info at https://ec.europa.eu/food/horizontal-topics/farm-fork-strategy_en

[4] https://ec.europa.eu/environment/strategy/forest-strategy_en

[5] https://ec.europa.eu/clima/eu-action/forests-and-agriculture/land-use-and-forestry-regulation-2021-2030_en

[6] Ecosystem Accounting, one step further to achieve the Green Deal objectives: https://www.youtube.com/watch?v=kSPqqmU9eSU

[7] https://seea.un.org/news/aries-seea-rapid-generation-natural-capital-accounts

GEO (the Group on Earth Observations ) is a partnership of governments and organisations envisioning a future whereby decisions for humankind will be informed by timely, reliable, openly shared science-based environmental information underpinned by systematic Earth observations. As an informal public, international body, GEO seeks to help its members (113 national governments) to understand how EO products and services can help them in their work.

EARSC is a participating member of GEO and works closely with the secretariat on various topics, but especially those connected with private sector engagement. The links with the private sector are important and the GEO Secretariat wishes to develop tools in the future to enable the private sector to engage more with GEO and national members. This is a win-win situation where industry can help governments to meet their objectives and develop their own business in doing so.

How can industry work with GEO?

The idea was first expressed during the GEO Plenary Session in Brazil in 2012. Seven years later, the GEO Associate Membership category has been created. With this action, the GEO policy framework structured the involvement of the private sector by “institutionalising the idea that the private sector was needed to be a partner of the GEO community”. GEO has built a culture that is welcoming a public-private partnership and has created an environment in which the industry has importance. One important initiative has been the launch of “the industry track” which first appeared during the 2019 GEO plenary week in Australia. This gave the delegates the first real opportunity to meet with industrial representatives in an organised and structured way. EARSC was very pleased to be able to support the Australian organisation Frontiers SI to encourage European participation and to jointly organise events to facilitate meetings between European and Australian companies.

In the recent eocafe, Ms Yana Gevorgyan, appointed as GEO Secretariat Director on 1st July 2021, confirmed that the Industry Track[1] is here to stay and will feature in this years’ GEO plenary. Ms Gevorgyan also shared with us her vision for the future of GEO and the links with the private sector.

Beyond the Industry track, new types of partnerships were created in 2019 with some of the larger technology providers. The GEO Cloud Credits Programmes[2] provided extended access to compute technologies for developing countries; it created a new community of technical users satisfied to get access to big earth data in order to develop nationally and locally relevant applications.

Ms Gevorgyan very much hopes that a “business to government” approach will be developed in the future: through engaging with GEO as a forum of governments, there is a possibility to create tailored services with public needs and have the public sector as anchor costumer. Even though there is an apprehension with the risk involved in making new investments, GEO is willing to work on finding solutions that derisk those investments. GEO plays the role of an enabler, a communicator, helping countries on how to develop capabilities using EO data. It is easier in Europe and in some other countries because the industry is already developed and is supported by policy makers and robust funding programmes. It presents more challenges in countries where there is not that infrastructure. In this case, GEO can “rely on their members to be the conduit and bring the industry representatives into the conversation”.

Ms Gevorgyan also talked about the tools to help small companies and launched the idea of “accelerators” that would bring government needs, local industry representative with GEO providing access to public data. They would also provide mentoring, coaching and training to bring all the ecosystem of stakeholders (scientific actors, governments, and companies) around the table and have a discussion.

The issue of seeking funding is essential in that regard: learning how to access to represent a major challenge, especially in countries where the use of EO is not easy. These accelerators are envisioned at a regional or subregional scale with the objective to seek funding in order to enable small and medium companies to develop solutions that can be market-ready or with a potential. In parallel, GEO is working to create a robust and systematic conversation with the finance industry, in order to ensure that the financing becomes available to solutions and businesses that are underpinned by environmental information and make easier the availability of these prototype services to get access to finance.

In doing so, it is crucial to bring user needs: the most important is to have a conversation with governments to understand their problems and turn them into solutions using earth observation.

As a trade association representing the downstream services sector, EARSC can support GEO’s activities in a number of different ways. By showing GEO as a platform for companies to get ideas, innovation, fitting the needs of various users, EARSC can encourage and participate to a better involvement of the private sector. To that end, participating in the Industry Tracks or other activities involving the industry, such as the Climate policy and finance workshop[3] is another important step. Ms Gevorgyan would like to “build out on the outcomes of these events and put in motion a systematic engagement”.

Finally, through EARSC’s work and experience, GEO can benefit from a better knowledge of the downstream services sector. It will surely contribute to bring the agility and the innovation of the industry to turn it as operational services for decision-makers and support GEO’s work and missions.

[1] https://africanews.space/events/geo-week-2020-virtual-industry-track/

[2] “Satellite data and imagery require large amounts of storage and processing, so it is key that developing countries make use of cloud computing and take their algorithms to the data, not the other way around, to effectively and efficiently use this data to drive better decisions.” https://www.data4sdgs.org/news/geo-aws-earth-observation-cloud-credits-programme-harnesses-big-data-decision-makers#:~:text=The%20new%20GEO%2DAWS%20Cloud,and%20outcomes%20for%20the%20SDGs.

[3] The Workshop was held from 21 to 23 September 2021 with entities providing finance with the industry being part of it; two days were dedicated to EO in support of climate policy and EO as a basis for climate finance.

The Earth Observation Downstream services industry is a cutting-edge and fast moving sector for which innovation is key to provide new products and services. As a result, research is very important for the development of the business and its competitiveness.

Horizon Europe is the European Union research and innovation framework programme with a value of €95, 5 billion for the period 2021-2027. Renewed every seven years, the programme was previously known as “Horizon 2020”. Aligned with the ambitious objectives of the European Green Deal, Horizon Europe will contribute to achieve a more sustainable and digital Europe. On 15th June 2021, the European Commission adopted the main work programme of Horizon Europe for the period 2021-2022[1]. The Commission is currently working on the first drafting phase of Work Programme 2023-2024.

A good understanding of the structure of Horizon Europe is necessary to foresee the opportunities for the EO sector. First, it should be recalled that Horizon Europe has three main pillars: Excellent science (Pillar 1), Global challenges and European Industrial Competitiveness (Pillar 2) and Innovative Europe (Pillar 3). Missions areas are actions across pillars intented to “achieve a bold and inspirational and measurable goal” in a certain timeframe with an impact for society and policy making. These missions are the following: Conquering cancer; Adaptation to climate change, including societal transformation; Healthy oceans, seas, coastal and inland waters; Climate-neutral and smart cities and Soil, health and food.

Under Pillar 2, the focus is on tackling global challenges and boosting the EU’s industrial competitiveness. This Pillar is composed of six clusters that are broken down into individual expected impacts:

- Health

- Culture, Creativity and Inclusive Society

- Civil Security for Society

- Digital, Industry and Space

- Climate, Energy and Mobility

- Food, Bioeconomy, Natural resources, Agriculture and Environment

Each cluster aims to deliver in different objectives, through a series of “Destinations” (technology sectors) described in the Work Programme. It is recommended to read the Destination’s description and visit the Tender’s portal to know more about the funding opportunities, the eligibility criteria and conditions.

During our EOafe dedicated to Horizon Europe, our speakers presented the funding opportunities offered by Cluster 4 (Digital, Industry and Space) and Cluster 6 (Food, Bioeconomy, Natural resources, Angriculture and Environment) more specifically.

Marjan Van Meerloo, Policy Officer at DG RTD, stressed that environmental observation (data and information) is of great value in assessing the state of the planet and delivering crucial information for the Green Deal. Environmental observation is cross cutting over many destinations and is complementary to other clusters, specifically Cluster 4. Destination 7 of Cluster 6 aims to ensure (better) accessible, interoperable, deployable or exploitable information, including decreasing in-situ gaps and ensuring availability. Also, the integration of earth/environmental information coming from different sources (space-based, airborne including drones, in-situ and citizens observations) with other relevant data to deliver input is necessary for shaping Cluster 6 policies. In this context, there is a strong link between this cluster and Copernicus, ESA’s Earth observation programme, GEO/EuroGEO and GEOSS.

In the Work Programme 2022 (Opening 28th October 2021 with a Deadline on 15th February 2022), the following calls will be of great interest for the EO downstream services industry:

- HORIZON-CL6-2022-GOVERNANCE-01-07: New technologies for acquiring in-situ observation datasets to address climate change effects (Innovation Actions –€20 million)

- HORIZON-CL6-2022-GOVERNANCE-01-08: Uptake and validation of citizen observations to complement authoritative measurement within the urban environment and boost related citizen engagement (Innovation Actions –€14 million)

- HORIZON-CL6-2022-GOVERNANCE-01-09: Environmental observations solutions contributing to meeting “One Health” challenges (Research and Innovation Actions -€10 million)

It is also worth adding that an “Infoday” session will be held at the end of October 2021 and more information is accessible by consulting the European Commission Factsheet on the Earth and Environmental observation.

Martina Sindelar, Policy Officer at DG DEFIS, then developed the opportunities under Cluster 4 “Digital, Industry and Space”, which focuses more specifically on the EU approach to technology development. She recalled that for the first time in the EU Research and Innovation programmes, the use of Copernicus and EGNSS is at the core of Horizon Europe and many calls offer funding to reinforce EU capacity to access and use space. In more than 100 calls across all clusters, the mandatory use of Copernicus and EGNSS is foreseen “if projects use satellite-based earth observation, positioning, navigation and/or related timing data and services”.

Cluster 4 aims at leveraging on Copernicus and EGNSS to bring benefits for companies and citizens while fostering synergies between the two flagship programmes and supporting the Green Deal’s objectives. There are many calls under Cluster 4 where Earth observation plays a significant role. Here are a few examples:

- HORIZON-EUSPA-2022-SPACE-02-52

Public sector as Galileo and/or Copernicus user

- HORIZON-EUSPA-2022-SPACE-02-54

Copernicus downstream applications and the European Data Economy

- HORIZON-EUSPA-2022-SPACE-02-55

Large-scale Copernicus data uptake with AI and HPC

- HORIZON-EUSPA-2022-SPACE-02-56

Designing space-based downstream applications with international partners

Furthermore, there are opportunities under the CASSINI initiative. Many tools offer support for companies developing applications using Copernicus and/or Galileo data by giving access to investment (Cassini Seed and Growth Funding Activity/ Matchmaking instruments) and supporting the development of the business (Cassini Business Accelerator, Cassini prizes).

Our discussion during the EOcafe emphasized the many opportunities across the different Clusters of Horizon Europe. There is no doubt that the Earth Observation Downstream services industry can benefit from the EU research and innovation programme, especially with calls under Cluster 4 and 6. We will look closely at the upcoming Horizon Europe calls to guide the companies and support them in their application.

[1] You can find here a previous EARSC Policy Blog about Horizon Europe Work Programme 2021-2022.

The digital economy is not only shaking up many sectors but fundamentally changing them! The result is the emergence of new innovative business models and opportunities for those who are able to embrace the change. The insurance sector is no different and a new approach is being developed by Skyline Partners.

Index insurance changes the way in which the risk is managed. Traditional insurance works through loss adjusters who are visiting the site of the damage after the event, to inspect and calculate the extent of the loss. This is an expensive process especially where the damage has occurred in remote areas. When travel restrictions exist, for instance in times of a pandemic, travel may simply not be possible.

Mr. Laurent Sabatier, Co-Founder and Executive Director of Skyline Partners, explained the principles of index-based insurance to us in the Eocafe on 27th May. Earth Observation (EO) gives the possibility of remote inspection, at least partially, of any damage – depending on its nature but index Insurance goes one step further. Instead of relying on loss adjusters to assess the value of the damage, a trigger is identified, and then monitored. For example, a property may be insured against a natural hazard such as a hurricane. A crop may be insured against freezing nights. In each case, payment will be made if a hurricane occurs or if the night temperatures drop below zero degrees. No loss adjuster is involved as the parameters insured are monitored remotely. The use of index insurance is becoming increasingly popular and represents an opportunity for the geospatial services industry.

As far as Skyline Partners company is concerned, they have been pioneering this new approach through the use of EO data. Whether the peril is a natural catastrophe, a pandemic or other measurable risk, geospatial intelligence is helping to insure this risk of damage to crops, infrastructure or people. This is opening up new opportunities for EO service companies and data providers which we explored in the EOcafe.

So the cost of managing the insurance risk is reduced, but what is the advantage to the customers? Does faster pay-out means a reduced pay-out? Not necessarily. In France, for example, lots of farms and vineyards have lost much of their business. Index insurance in that case, can potentially help to get protected even before these risks happen. In fact, they are predictable. It is possible to build the infrastructure to protect the products under index insurance for preventing risks. The objective is to complement ex ante products with a proper infrastructure, this can even be possible with a pay-out based on a signed contract.

Spatial data is an integral part of index insurance by design. In fact, an index is based on data exploitation and satellite data is a fundamental part of it. Technical failure can be avoided with satellite data and imagery based on the index. An index is systematic and there is still some work to be done with collecting data and building new algorithms.

In terms of data differentiator, the most important and critical criteria is the granularity aspect of data, as the specification of the data is what makes the product possible and therefore the growth of the service of index insurance. Guaranteeing this, you ensure the growth of the business.

The competition aspect related to the business continuity is based on trust, as the risk is based on its performance. In the meantime, space institutions which are furnishing geospatial data, will not disappear. That is a very important aspect for the continuity of the business.

It is always preferable to use synthetic data as they are easier to scale up, but it also depends on the needs. In terms of timing for example, forecast and temperature data, at the moment being, are very predictable. An element of identification is available in the short term. Here the index industry has a role to play.

Buyers of index insurance are direct companies facing the risks, such as farmers; for each seller, there is a buyer. But the farmer is the one who is benefitting from the service even if it is not the buyer directly. In this case, the remote sensing industry has an important role to play as supplier and intermediate. This is how the market share could work and this is the customer base.

The aim is to create an upfront evaluation before the risk happens, this is why data collected on the ground is also very important to validate the index. This is why the basis risk can be very different.

Overall, index insurance looks to be an interesting area for EO suppliers to follow and opportunities should arise. One way to follow progress is through the FIRE project led by EARSC, where insurance is one of the focus topics. The FIRE forum, to be held next week at the time of writing will be a public opportunity to do so.

Aaron Scorsa & Geoff Sawyer

The EU Green Deal sets out a highly ambitious plan to preserve our planet and to promote Europe as the first climate neutral continent by 2050. It includes objectives to decarbonise the EU economy, revolutionise the EU’s energy system, profoundly change the economy and inspire efforts to combat climate change. It foresees a sustainable economy in this timeframe with a number of intermediate targets being set for 2030.

The EU budget together with the Recovery Plan will provide the finance to support these goals. The Green Deal is a cross-cutting, overarching ambition which will be realised through many different policies and programme elements. The research budget -Horizon Europe – will be a core part of the jigsaw puzzle of elements which will go towards helping Europe achieve its goals.

In the EOcafe of 29th April we welcomed Dr Anastasios Kentarchos who is Deputy Head of the Ecological and Social Transitions unit in DG RTD, who joined us to discuss and to help us understand the big picture portraying the Green Deal and the relevance which R&D activities will have. He started off by explaining that the Green Deal is for everyone. It is an inclusive programme and that no-one should be left behind.

The Green Deal has provoked a very big change in the way that we think about issues in Europe. Before, discussions were about either competitiveness or about sustainability; the green deal seeks to reconcile these two sometimes conflicting, perspectives. It is important to understand that it is not simply a new environmental policy.

The Green Deal rests on a series of tranformative policies. In addition 3 cross-cutting elements acting as key enablers are important to note : ; i) international as it is a global effort where global alliances and aligned efforts will be essential, ii) an EU climate pact so that everyone is engaged from citizens to communities and organisations, and iii) R&I which will underpin and inform much of the effort. There is a strong need for Innovation (both technological and non technological), sparking new ideas.

The new European climate law, which is at the heart, enshrines the 2050 carbon neutrality target as well as an intermediate 55% target (referred to as “fit for 55”) in 2030. The EU climate adaptation strategy will include measures to increase resilience and prepare for unavoidable impacts. Many EU policies will be affected, including; investing in more sustainable transport (cut transport emissions by 90% by 2050), striving for greener industry, eliminating pollution, making homes energy efficient (targets include 100 climate neutral cities), sustainable agriculture (from farm to fork), protecting nature and promoting clean energy. Supporting these active policies will be new financing schemes, legal frameworks and ensuring it is fair for all. These were all described in more detail by Dr Kentarchos and explained in his presentation slides.

A new industrial strategy is to be published in early May which has taken many months to develop. This also reflects in part the conflict between sustainability and green growth and has led to a long, and sometime difficult debate in the EC. The strategy is also addressing 14 industrial ecosystems in areas related to mobility , energy, agri-food, steel, textiles, as well as digital industries. It will change the paradigm for big industrial players in Europe, going hand in hand with the circular economy action plan which seeks to change the way we produce and consume through the product lifecycle.

Decarbonisation has to advance rapidly; up to 5 or 6 timers faster than today if the 1.5degree challenging target from the Paris agreement is to be met. Regulation is important but will not be enough. Innovation is strongly needed as well. Europe filled the gap left by the previous US administration but are happy now that we are speaking the same language with the Biden administration.

The European Green Deal is a major machinery, major political initiative from the EC. Together with the digital initiative represent the 2 heavyweight policy initiatives from the EC. A large part of the EU budget for the next 7 years will be turned towards the Green Deal. Funding will consist of 30% of the next MFF and Next generation EU (combined these have a total budget of €1.8t) and 37% of the Recovery and Resilience Facility (€672m).

A new approach is expected for R&I with a strong commitment to a cross-cutting approach. First Green Deal call was launched under H2020 as a means to test the approach. Spending €1b in 3 months was a challenge but it has given extremely useful experience and guidance for Horizon Europe. This has been tested as a model for future calls especially regarding the cross-cutting research. Focus research where there are policy needs. Other calls will focus on bottom-up research. Various instruments are available; partnerships and the EIT (European Institute of Innovation and Technology) already exist, to these are added the new European Innovation Council and the data and digital infrastructure in support of ecological transition.

The EC has also launched 5 Missions of which 4 are directly relevant:

- Adaptation to climate change and societal transformation

- Climate-neutral and smart cities,

- Healthy oceans, seas, coastal and inland waters

- Soil health and food.

The Missions are not just R&I instruments but rather public policy initiatives with concrete milestones.. The mission-led approach is a new concept to be piloted in this Framework programme (Horizon Europe). Their aim is to give European citizens the vision of large societal goals which will shape the Horizon programme and associated policy. Even if they have been developed by DG RTD they are not to be run from there. Boards are established for each mission comprising senior officials from each of the relevant DG’s and which are chaired by the most relevant DG ie for climate change adaptation it is DG CLIMA.

Then there is a second level of governance which is there to enable co-ordination between the different instruments. In this case, for example, the mission on cities should be co-ordinated with partnerships linked to industry. Finally, a third level of governance will ensure co-ordination with the activities carried out in the Member States. For example, the 100 cities selected will define their plans which should then become a firm agreement between the city, its Member State and the Commission.

There are also major change in implementation of the Horizon programme. Previously, DG RTD (and RTD-family DGs) were at the heart of drafting calls or co-drafting in some circumstances ie for energy and mobility. Co-creation by a group with representatives from all DG’s, brings together research expertise with policy expertise. It means that the task is harder but the final product is better. It is seen as a co-operative exercise and nobody really holds the pen. The first calls of HE are drafted but awaiting the overall political agreement (MS).

Emmanuel Mondon asked a question concerning the links with the digital transition and especially the creation of data spaces. Need to ensure links with policies and services ie climate services. Difficult to achieve the translation between innovation and services. Innovation becomes real when the results find a place in the market. Calls will be about how EO can add value to policies. Example Amazon, Apple have not created technology but new business models.

The work to date represents the design phase and we are now entering the implementation phase. This will bring its own new challenges both positive and negative. It is an important opportunity for the EO sector which will now seek to play an appropriate part as the programme becomes established.

For further information, refer to our previous blog on the Green Deal and watch out for future EOcafe's as we explore aspects of the plan in more detail.

Geoff Sawyer

Celebrating our first anniversary we returned to the evidently popular subject of the use of AI technology for Earth Observations. In a previous EOcafe on the 4th February, we heard from the AI4EO project which is one of many springing up with different sponsors at European and national levels to promote this synergy between technologies. There are many initiatives[1] and one of our aims in EOcafe is to try to help clarify this somewhat complicated landscape.

Our focus this week was the initiative AI4Copernicus which is a newly launched project under Horizon 2020. The project manager, Vangelis Karkaletsis (Director at the Institute for Informatics and Telecommunications at Demokritos), explained the structure of the project, its partners and the links with some of the other initiatives especially the DIAS and a second H2020 project, AI4EU. AI4EU involves partners from research and industry aiming to deliver research and innovation in AI. It is a broad programme spanning many different sectors to which, AI4Copernicus seeks to add EO services. One key deliverable is the provision of a catalogue of AI resources and tools, an experimentation platform, a content manager system for AI events and open calls. AI4Copernicus partners include companies involved in 3 of the DIAS platforms, public institutions and research institutions to enable AI and EO innovation.

A key goal of the project is to provide a bridge between Copernicus as an EU flagship and its data and services available through the 3 DIAS and the resources available under the AI4EU. As expressed by Vangelis, to make the AI4EU AI-on-demand platform, the platform of choice for users of Copernicus data along the value chain (scientists, SMEs, non-tech sector). The Dias’ Creodias, Mundi and Wekeo are all represented amongst the project partners. AI4Copernicus will provide support to teams creating new services which will be installed on at least one of the 3 DIAS.

Xenia Ziouvelou, (Research Associate at NCSR Demokritos & Lead of the AI4Copernicus Open Calls) explained how the project will launch calls for new services integrating EO data, and AI technologies. An important contribution of this project, as Xenia mentioned, is the possible creation of new ecosystems as a result of by bringing together these communities, including technology advancements, new markets, at innovation and industry levels.

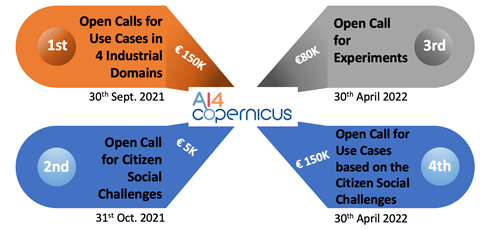

Xenia explained that there will be 4 rounds of calls, the 1st call will be for use cases in four industrial domains in the areas of energy, health, security, and agriculture domains. The 2nd call is to be focused on citizen social challenges, the 3rd call for experiments and the last call on use cases based on the citizen social challenges. AI4EU will provide cloud infrastructure for the successful applicants and also create instances inside the DIAS platforms to enable the successful candidates with data sets access, cloud, and services among some tools. Regarding the financing, Xenia mentioned for the first round of calls it is provided a 100% funding for a two or more partner consortium of up to 150,000 EUR per project. Important to note that the consortium must have a partner with at least some expertise on AI to assure the running of the project.

Responding to a suggestion from Alberto MenVangelis agreed that this is a good example of a new tool that could be installed on a DIAS platform and made available through AI4EU (or vice versa). This could then be used by many new services as a building block. He mentioned as an example the existence to populate tools demand applied to this case could be the use of tools of the AIEnergy project, which is one of the ‘sister’ projects and how its datasets can be used as well for AI4Copernicus.

Geoff asked about the sustainability of the AI4EU platform as the project ends in less than 9 months time (end 2021)? How can challenge winners be confident that effort invested in installing their applications on either DIAS or AI4EU will still be supported in 1- or 2-years’ time? Vangelis explained that this is currently being studied but that the leader of AI4EU, Thales, is committed to keeping the platform running. The AI4Copernicus project will contribute to the sustainability by enriching the set of tools which are available. Research projects are expected to contribute more tools which will extend the AI4EU platform and ensure it is used by other communities. In terms of the funding to secure this, it is not yet clear, but it is foreseen to establish a foundation and more details on this will be worked out in the next few months.

Four partners in the project are potential users of new services. Richard Hall (Equinor - a leading energy company) outlined some of the questions which he would like to be addressed through challenges and that there are links between the 4 sectors to be addressed: For instance,

- Energy and health, how do the activities of energy companies’ impact on the health of a city?

- Energy and security, how much energy can Europe produce? Where is it needed or will be needed in 50 years time?

- How can EO and meteorological data be used to optimise the cleaning of solar panels from dust and particles gathering on them?

Vangelis confirmed that questions like these will be included in the calls as a guide to those responding.

Vasilis Baousis from ECMWF introduced his view of the project with both the use of data from CAMS and the use of the DIAS WEKEO where ECMWF is a partner with Eumetsat and Mercator. Vasilis also cited Destination Earth as another future resource and source of tools and data. Vangelis also pointed out the link with the AI4EO project through ECMWF which is driving their first challenge launched by this other project.

Michele Lazzarini from SatCen mentions that security is an important domain with possible applications connected to other sectors. For this, SatCen is currently drafting its calls based on security needs and the interaction with other sectors (e.g. climate).

Vangelis summarised with a reminder that funds are available! The first calls will be launched in June/July with a deadline to respond by end-September. The 6 selected projects, each for up to €150k, will be launched in January 2022. Good luck to everyone!

Geoff Sawyer & Sandra Cabrera Alvarado

[1] AI4EO (ESA), AI4EO (EC), AI4EO (DLR), AI4EU (EC), AI4Copernicus (EC), AI4Copernicus (Copernicus Relay in Wallonia and Luxemburg), AI4GEO (CNES) and many more.

How can we help the media get better use of EO in its progressive use? This was the main question raised by Geoff while opening this EO Cafe. Since the launch of Landsat (1972) followed by SPOT (1986), EO has been used as a tool by journalists to show the readers of the days’ newspapers i.e. the main-stream media (MSM), images of the Earth to illustrate their stories. Never seen before, these images were highly educative and certainly led to a much greater awareness of geography and local news amongst the wider population. However at the time, these tools were costly depending on the resolution and provider.

Today, on the other hand the offer has changed. Public and commercial EO satellites offer free access to images as a way to promote their capabilities, making satellite imagery accessible to journalists. For example, Twitter recently featured satellite images of the EverGiven container ship stuck in the Suez canal using several types of imagery and providers. EO imagery is now often used by journalists to provide depth to the story by illustrating it and enhancing interest worldwide whilst providing to readers new perspectives, illustrating events or showcasing remote areas.

Each of the main (optical) satellite operators has a media office that works closely with news outlets to on the one hand support the storytelling and on the other to promote their capabilities – as well as developing a philanthropic image. Hence the mix of promotional commercial imagery and free public data coming from ESA, NASA, ISRO and other agencies, supported in some cases by extensive analytic capacity is keeping news sources satisfied. Important to say also that today a lot of the focus has moved away from the MSM onto social media – even for the traditional publishers. The digital version has become the reference even if a paper version is still published. Added to this we have social media that also act as new online media channels like Twitter, Facebook, Instagram, etc.

According to Jonathan Tirone, News Editor from Bloomberg, who was a guest in our recent EOcafe, EO imagery is bringing a new language to the media as it becomes much more widely accepted in newsrooms. Jonathan gave a number of examples including that of the Gchine uranium mine in Iran. This had been the subject of some detailed analysis showing how Iran had reopened the mine contrary to international agreements and, more particularly, had built facilities to process the ore. He observed also that Google Earth had played a strong role in warming up the news editors due to its easy access offer to satellite imagery with enough resolution. This is the case of the Copernicus Climate Change Service, which Jonathan mentioned, which has revolutionized the open-source platforms on coverage of climate change in Europe due to its free access. Nowadays the access to data is not an issue as before but Jonathan stressed out expertise is needed for an accurate interpretation and give the image an accurate context while doing the storytelling.

It is precisely this need that Jonathan notes it has originated a need in remote sensing analysts describing it as a “discrete“ industry in the bloom that has awakened the investors‘ interest. Another trend he pointed out was the need for the use of new technologies, such as big data tools for reporting as well as AI analytics. Most likely the next generation journalists will know how to combine techniques of writing, video production and use of technology as tools to enrich the newsrooms.

In addition, the immediacy of news reporting today is fuelling demand for instant reactivity from image providers as Remco Timmermans (#timmermansr) mentioned, who was our other guest in this EOcafe, and who, in 2020 was designated the #EUInfluencer for space. Remco presented the use of EO in the media from another angle. The use of EO for examining the veracity of reporting events. He called this “investigative journalism“ where journalists take in situ images from social media and prove its veracity by comparing them with satellite images for this fact-checking. As an example, he talked about the case of the Syrian war reported by Bellingcat “spaceproofing” what occurs on the ground.

Remco illustrated this with the examples from the EverGiven and the succession of images from each operator appearing on Twitter. These gave a fantastic opportunity to compare the images and not just those from optical satellite! After Sentinel-2, which set the scene, we had images from Planet, from Maxar (GeoEye) and from Airbus (Pleiades) showing in increasing detail the stuck ship and the efforts to release it. Maxar had the chance to have a satellite within range at the time the ship was freed demonstrating the advantages in having constellations and multiple imaging opportunities.

Both Iceye and Capella space released radar (SAR) images of the ship taken at night to illustrate the advantage that radar offers. These also illustrated the different features which radar highlights and hence the need for expert interpretation. For example, the foreshortening effect caused by the different image properties needs to be well understood – but then can be very useful and provide completely different information.

Does the industry support the news in this reporting effort? Jonathan mentioned that EO sometimes is a fairly tight community with limited possibility to bring expertise to interpret data for news purposes. On the other hand, Remco proposes a solution to this need of technical skills by mentioning imagery platforms such as the Sentinel Hubs make available processed imagery that could facilitate its distribution. This raises the question if whether in the future, this should be part of journalistic training. However, indeed these portals are not necessarily intended for journalism purposes as pointed by Remco. On the other hand, the friendliness or usage of platforms still remains subjective and even debatable, what it is not is the possibility of journalists to seek EO specialists and more continuity in satellite imagery supply.

Remco also provided a list of some of the more important influencers on the subject of EO, several of whom were in the audience. Geoff Smith (#DrGeoffSmith) one of the influencers identified by Remco, asked if information products or an optical image was better? The answer was it depends on the scope of the work but most importantly on the targeted audience. Whereas a remote sensing specialist would like more detailed technical information for decision making, an optical image will be better for a general audience visiting social media. Remco mentions this as “humanizing data” to civil society, in general, is the best option to showcase the benefits and opportunities of EO.

Stephane Ourevitch (#ourevitch_stp), and who is very active on Twitter behind the DG-DEFIS (#defis_eu) account, considers that the tools are out there which journalists can use. With no background in remote sensing, Stephane finds the Sentinel Hub (#sentinel_hub) a relatively easy tool to use to gather images to support stories. This led to further discussion concerning the training of journalists or support from the EO services sector. Remco also identified Pierre Markuse (#Pierre_Markuse) author of a useful guide for journalists[1] and Ground Station Space (# Dot_Space) which he supports as good, reliable resources.

This information brought by journalists also faces the issue of “fake news”. Dietrich Hans who was part of the audience raised this pertinent topic by presenting the possibility of a satellite image being misused to create misinformation. Jonathan shed some light by commenting the more sensitive the story or topic is a higher level of analysis is needed. Indeed, depending on the topic, further investigation is needed and crucial, rather than just using satellite imagery as the main evidence, such as the case of the Iraq war in 2002 used as main proof by the US and remains debatable. However, this further investigation remains a pillar for journalists, where, in this case, satellite analysis must be supported by other sources to be used as a reliable source of information.

The intervention of our guests showed us the two sides of how EO can be used in the newsroom, either as an illustration and scene setter with the image attached to the story or in the form of investigative journalism. Whether a need to set up a mechanism to have access to a remote sensing specialist remains a question that possibly in the future needs to be addressed to assist the journalist sector in their uptake of EO to be used in an ethical and responsible way.

Sandra Cabrera Alvarado & Geoff Sawyer

For further reading:

Space race over the Suez Canal see groundstation.space

Pierre Markuse “Satellite Image Guide for Journalists and Media” provides an overview and some tips on how to use/create satellite images for media.

[1] Pierre Markuse “Satellite Image Guide for Journalists and Media” provides an overview and some tips on how to use/create satellite images for media.

Playing games is a an extremely old pastime but digital gaming – which is what is generally understood by the term – is new. Whilst gaming is big business, the imaginary world of games may not seem the obvious place to take real images of the Earth. But for a few companies it is and there is some very interesting business going on to bring these two worlds together.

One way, the most obvious (perhaps) is to use EO images as a backdrop for the game. This is the case with the Microsoft Flight Simulator which we understand is now using Sentinel-2 data to provide the terrain over which the aircraft is flying.

Another approach is to use gaming tools to support data gathering. One popular example of this is the globally popular PokemonGo which is offering in-game incentives for users to open their cameras to the developers with which they can build 3D models of real locations. The business model is primarily based on advertising linked to the location. No EO is involved in this example.

Other companies are taking more modest steps to use the EO imagery as a tool to collect data linked to agriculture, cultural heritage and other applications where local data enhances the results. By linking this data collection to gaming, it can appeal to the younger generation (but not only!) and turn a useful tool into a pleasurable (for some) pastime.

The gaming sector is enormous business with around 1 to 2b players around the world yielding a business sector worth an estimated $200b per annum. In the free to play segment, where advertising drives the revenues, the market is 25% or $50b per annum and growing at around 12.5% each year – similar to the EO services market.

To explore this topic further and how EO and gaming relationship arises, the EO Café introduced three guests working in this domain; Hugo HERNANDEZ, Co-founder and CTO of World Game, Hans VAN’T WOUD, CEO and founder of BlackShore and Tomas SOUKUP, Project manager at GISAT.

Hugo HERNANDEZ - Co-founder and CTO of World Game based in Paris - comes from a gaming background. He talked about Impact Gaming which is his approach where the games’ purpose is to collect and analyse data, but which also has other purposes, such as raising awareness to societal topics, and crowdsourcing of solutions by working with different industries. Just a few of their games are working with EO and it is a new area which he hopes to explore further.

Tomas SOUKUP- Project manager of GISAT from the Czech Republic - explained how his EO company entered into the gaming sector starting with the an ESA project GAME.EO. By using mobile-based tools for supporting crowdsourcing campaigns and gaming approaches for monitoring informal settlements (slum areas) applied in developing countries. Based on this experience, Tomas foresees a great potential with these synergies.

Hans VAN’T WOUD - CEO and founder of BlackShore in the Netherlands– presented several games he is producing using EO satellite imagery for several applications. Here there is a very strong emphasis on the use of imagery as the basis for a game to analyse imagery – a sort of crowd analysis. Gamers are encouraged to classify images and are rewarded according to peer results. The gaming is free but has a social motive concerning smart agriculture to disaster monitoring transposed in a gaming context. The detailed maps that result are not available through other sources (Google, OpenStreetMaps etc) and are valuable for NGO’s and International organisations working in remote regions. Hans explained how he is exploring other ways to monetise the games through prizes, fees for in-game purchases and straight donations.

We discussed also the relevance of AI. Hugo commented this technology can complement the gaming products. Tomas concurred that AI process can even stimulate and improve processes such as automatic recognition features and with this supporting human tasks.

On co-creation, Hans uses this feature in his company’s games by requesting the public to assist for certain causes, for example in developing countries, crowd mapping is very demanded based on EO satellite information.

The younger generation spends a lot of time gaming, as Hugo mentioned, and this can be used for learning. All speakers agreed that this can be used in a positive way as an opportunity for educational or public awareness. Virtual or Augmented Reality are also technologies which can be highly relevant. Tomas followed up by saying this opportunity should also be used as a tool for further exploration of data usage. As in many markets, partnerships are very important, and all the presenters are seeking opportunities to explore this further and expand their presence in the gaming market.

Sandra Cabrera Alvarado & Geoff Sawyer

The European Commission has set out an ambitious goal with its 6 priorities in its own 5-year plan (2019 – 2024). The Green Deal has the objective that Europe becomes the first climate-neutral continent by 2050 by making its economy sustainable. How can the EO industry play a role in this transition and where will the opportunities emerge? This is the overarching question this EO Café addressed which was discussed by me and our two guests Ricardo CONDE, President of the Portuguese Space Agency and Agnieszka LUKASZCZYK, Senior Director for European Affairs with Planet and Director of EARSC.

The Green Deal will have many components, will be implemented using many instruments and many actions will be taken to move towards this goal. Many existing policies will be revised to reflect new actions or more ambitious targets. New or strengthened measures to monitor and control actions being taken which will require new reporting. New technology will be developed through Horizon Europe and its successors and R&D can be expected to be a strong component. The means for this will come from a number of budget lines including the European Recovery Plan. This high degree of complexity means that this one EOcafe can only start to look at the subject and future EOcafe meetings will take some specific aspects to go into more detail.

Ricardo CONDE -President of the Portuguese Space Agency- confirms the Green Deal relies on many cross sectors, to achieve its goals and create a common understanding amongst the member states while creating harmonised environmental policies. For this, the development of environmental applications using EO data is currently needed and yet still lacking in the downstream sector at the moment. One barrier is access to high-resolution EO imagery. Removing this barrier would mean that not only in Europe but worldwide, more EO sources can be accessible to various sectors to monitor these environmental concerns. In consequence, business models need to be changed to have the possibility to develop more applications in the downstream sector.

Agnieszka LUKASZCZYK- Senior Director for European Affairs with Planet and Director of EARSC- explained how EO and also the EU EO programme Copernicus can contribute concretely with the Green Deal policies[1] to be tacked by member states using EO imagery. In addition, the EO industry can foster synergies with other technologies such as AI and Big Data to be provided to governments as a tool to support their decision-making process. Thus, private-public partnerships (PPP) play a key role in this environmental case. For example, Agnieszka introduced several partnership mechanisms where the environment and EO sectors meet. One of them was the creation of a Geospatial centre under the basis of a PPP, where a central hub located in the EU can provide to the Commission monitoring tools for priority policy areas. Another idea mentioned was the establishment of a Commercial App Ecosystem by making available environmental apps.

The audience pointed out as well another key aspect which is the end-user or the customer. In order to shape the PPPs and foster the EO-environmental synergy, it is crucial for the industry to understand who the customer is and what are his/her specific needs. For example, to develop more dedicated environmental services, besides the existing ones provided by the Copernicus Climate and Monitoring Services, the industry needs to know precisely the customer’s needs and even pay more for specific satellite data to develop dedicated services and with this, reach that extra mile.

An important point raised by Agnieszka was the fact that public and private services should be complementary and not in competition. There will be public needs that only the public sector can provide, and a similar case as the market opportunities with private services provision. Copernicus Services can always be complementary to the ones offered by the industry regarding the environmental sector, as it is well known that the more sources the better quality of apps and services will be.

One important component of Green Deal is the future European Climate Law (proposal drafted in March 2020) that will make binding the overarching goal for Europe’s economy and society to become a net-zero greenhouse gas emissions by 2050. This means the ambitious goal of cutting emissions, investing in green technologies and protecting the natural environment in the EU. In addition, this Climate Law aims to ensure that all EU policies contribute to this goal and that all sectors of the economy and society play their part. Earth Observation technologies can be useful and even essential to achieve the complex and ambitious goals of the Green Deal and possibly to support the future European Climate Law.

Another element to consider is how the EU’s Destination Earth (DestinE) and ESA’s Digital Twin Earth can support the New Green Deal goals? There is still no clarity on how these space-driven programmes will work and contribute to other EU policies. Regarding the international sphere, it was made clear that the New Green Deal should be used as a diplomacy tool where Europe can position itself as a key player not only in the environmental sector but also disruptive in the EO sector if these two forces join.

The European Green Deal cannot happen in isolation and will require and will affect many international relations. Synergies and international cooperation are crucial to tackling climate and environmental challenges as these are clearly not a domestic or regional issue but a global problem that has been shown by COVID-19 pandemic and the sanitary situation the world currently faces. Some of the geopolitical aspects of the policy are addressed by Bruegal in a recent paper.

Having tried to expose a wider perspective of the Green Deal, EOcafe will meet again in the future to go into more detail of various aspects. In the near future, we plan to look at it from the R&D perspective and the priorities of the Horizon Europe workprogramme. This will include the “Mission Areas” which includes the one on climate adaptation as well as others that will be relevant. All stakeholders from the EO and non EO value chain, from the public and the private sectors, can play a role in more efficient protection of the environment.

Further reading:

A plan for the future of the planet by European Investment Bank (Climate Bank Roadmap): https://www.eib.org/en/stories/climate-bank-roadmap

The geopolitics of the European Green Deal published by the Bruegal Group

Sandra Cabrera Alvarado & Geoff Sawyer

[1]1) Food production policy under the ‘Farm to Fork’ Strategy, 2) Preserving and restoring ecosystems by stopping biodiversity loss, forest restoration and protection, and 3) sustainable and smart mobility

In the EOCafe, “where the EO Community meet”, our subject for discussion had a more applications driven focus. This time it was dedicated to the use of EO information for the raw materials sector. “Raw materials” includes mining but also other means of extraction and even recycling as a means for production. Although, for the EO community, it could be obvious that EO data/information is useful for mining companies in several of its stages of operations, (from the exploration phase, environmental assessment & permits, to design, operations, mine closure and aftercare), for the mining sector there is still a long way to go for this relationship to succeed.

Margreet Van Marle, Consultant of Wildfires and Climate Resilience at Deltares, introduced the ESA funded project EO4RM project, which is a “best practice” project building upon the model which was successfully developed with the Oil and Gas sector some years ago. The best practice process identifies the demand through a list of challenges which the sector face. It then looks at what EO services can help overcome those challenges and subsequently the gaps and the barriers to uptake in the sector.

To put this into perspective, Reinier OOST, Product Lead at Sensar and Brendan Morris, Managing Director of LTMS (Lisheen Technical & Mining Services) gave examples as showcases. These showcased 15 EO products and their potential for the mining sector, including monitoring of tailings, subsidence monitoring of open pits and detection of environmental damage.

Even if EO technologies are not unknown to the mining industry, and especially the larger companies, there is still much room to increase their use, mainly through raising awareness of EO in the medium and small companies who have no knowledge or access to EO data according to Reinier. Once more, the main challenge EO technologies faces is awareness of EO and its capabilities along with the need of skills and expertise to be built within the mining companies. However, they are not the only ones. To go deeper, Margreet explained that even if an EO company with expertise provides high level products but does not understand the demands of the mining company, then the product will not fit the needs and meet the mining company needs. Vice versa, if the mining side lacks skills and knowledge, it will be challenging to make accurate requests, as its understanding in the EO technology such as processing, and interpretation of imagery could represent a barrier to procurement. According to Reiner, the image of EO in the mining sector is still science and research-based. Whilst this might have been true 10 or more years ago, the EO sector is now much more business orientated.

Reiner mentioned regulations as a driver. If norms were put in place under a regulatory framework at an EU level, this could enforce the predictability on mining management with the use of new technologies, amongst them EO, that is not there at the moment. In addition, the audience raised the topic of safety as an important topic in the mining industry, which should be put more attention worldwide as a legal obligation for the industry to invest in technologies to guarantee safety monitoring approaches.

Although international policy actions on safety are in force, these are under the umbrella of environmental protection, such as UNEP setting global environmental agenda including sustainable mining, the use of technologies for personal safety is still weak. For the record, the EU counts with a Directive[1] establishing minimum requirements for improving the safety and health protection of workers, however, it dates from 1992, which consequently EO technologies are not considered as a resource to enforce this legislation. It could be time to consider the use of EO in another piece of EU legislation to improve its enforcement.

Validation emerged as another barrier for the sector i.e. how can the products and services be shown to meet acceptable standards. Data is needed on a global basis to raise confidence in the services which are offered. Both some form of certification of the processes as well as validation of the satellite data will be necessary.

In conclusion, the main question is how these two sectors can develop a more fruitful relationship? The aforementioned oil and gas (O&G) sector created an informal advisory group with the EO sector called OGEO and which later became a sub-committee under the O&G umbrella association the IOGP. Can similar structures be envisaged under the mining and raw materials sector? Both Reiner and Brendan thought that this would be possible under either a European or International umbrella – which seems like a good recommendation, endorsed by the EOcafe participants, for the next steps.

Geoff Sawyer & Sandra Alvarado

For further reading:

Mineral Exploration from Space

https://www.esri.com/about/newsroom/arcwatch/mineral-exploration-in-the-hyperspectral-zone/

[1]See Directive 92/104/EEC https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:31992L0104:EN:HTML

Approximately 180 attendees gathered on the EARSC second EOcafe of 2021 to learn more on how Artificial Intelligence (AI) can help improve and interact with Earth Observation (EO) services. Both of our invited guests represent the community of AI developers and the community of EO service companies to give a wider perspective on the topic.

Nicolas Longepe - EO data Scientist in the European Space Agency’s Φ-lab (Phi-lab)- explained how the ESA Φ-lab provides the platform for companies and individuals to become more familiar with EO services and especially to bring new technology to bear upon the sector. The recent focus has been on AI and new missions even sometimes combined. This has led to establishing the AI4EO project initiative. Nicolas also cited the In-cubed programme as of possible interest for those seeking to develop new activities/products together with ESA’s help.

Annekatrien Debien -Head of the Brussels office of SpaceTec Partners and lead of the AI4EO project- considers that bridging the two communities is not an easy task. In fact, the AI community is very diverse since AI is a transversal tool. Why? Due to the mix of industrial and research experts in the AI community. It is clear that satellite images are not just a picture from which you extract only one parameter, but a complex dataset that aims to tackle complex challenges that can actually profit from AI community knowledge.

All of the datasets taken from the satellites could get some insights on the parameters using AI. Thanks to AI, in general we are talking about prediction, detection, classification, big data analytics and super resolution emulation. Therefore, there is knowledge in both communities that can be complementary. However, one of the main challenges is to bridge the gap between the AI and the EO by fostering its use for example in the scientific community.

Dealing with EO problems, AI can be considered as a transversal and beneficial tool for EO contributing with all its techniques. For example, CNN (Computer Neural Network) which is adopted for segmentation (SAR) or GAN (Generating Adversal Network) for synthesizing images, mostly based on computer vision technics. Nevertheless, although a lot of different functions are already used there is still the need to explore them as only a small part of AI techniques are used. Linking the communities, finding partners and expertise remains the main challenge. To address this, Annakatrien currently the first phase is to build awareness in both communities to introduce both technologies. In addition, she explained the AI4EO challenge on air quality monitoring using Sentinel data promoted by ECMWF[1] is currently open and encourages the industry to submit its applications.[2]

Another issue perceived by the audience is the existing limitations on the robustness of the techniques and how both communities can benefit from their experiences to overcome such limitations. In addition, big data management should also need to be taken into consideration and the cloud solution, linked to the need to sustainability. This is illustrated by the use of Google and Amazon platforms and the place that the DIAS can play to address this demand. The audience also pointed out a limitation which is the lack of governmental research and data to reach a better understanding on how to get open tools, such as machine learning to explore the access to data, while academic and industry work are available.

Prompted by many questions from those in the EOcafe, Nicolas recognized that there should be more training efforts to provide access to data and other capacity building activities to raise awareness on AI and other technologies which is also a subject of interest for the Φ-lab. On the same line, the attendees also expressed their wish to know more on AI data trainings and object identification in AI and EO resolution gap. Trust on algorithms was a possible answer by Nicolas to start to resolve this applicability between these technologies.

Despite these concerns and issues raised, it was pointed out that there are already applications using AI in the EO community using models or algorithms with several levels of maturity that could be taken into consideration for the future of EO and AI possible synergy.

Finally, several attendees took the opportunity to promote resources and future events:

- Workshop under the EO4GEO project on 2nd March[3] (Daniela Iasillo).

- AI toolbox available called AiTLAS[4] (Dragi Kocev – Bias Variance Labs)

- A session on AI planned at IGARSS 2021 (Vasilis Kalogirou – EU SatCen).

- Machine Learning Datasets Library[5]

To assist AI and EO communities on fostering partnerships please write to AI4EO via the website[6]. Any EARSC member wishing to get involved can also contact the secretariat who will be pleased to help where possible.

Sandra Cabrera Alvarado, Aaron Scorsa, Geoff Sawyer

[1] European Centre for Medium-Range Weather Forecasts, [2] For applications submission visit: www.ai4eu.eu, [3] See www.eo4geo.eu ,

[4] See https://github.com/biasvariancelabs/aitlas/, [5] See https://www.paperswithcode.com/datasets, [6] For applications submission visit: www.ai4eu.eu

The first eocafe of the year 2021 provoked a great deal of interest with over 200 joining us in the virtual cafe to hear about the new European Union Agency for the Space Programme (EUSPA). It is fair to affirm that the (European) space community is eagerly awaiting the entrance of this new player and its influence in the future of the EU space programme activities, especially for Copernicus. Once the new European Space Legislation is adopted, the current European GNSS Agency (GSA) will be transformed into the EUSPA with its responsibilities extended beyond the current role of market development of EGNOS and Galileo:

- Fostering commercial use of Copernicus,

- Federating the user requirements for Govsatcom[1] and SST[2].

- Maximising synergies in the field of space innovation.

Fiammetta Diani, who is the Head of Market Development Department of the European GNSS Agency outlined what will be the role and mission of the new EUSPA according to the EU regulation proposal. In the EU space programme’s governance scheme, EUSPA’s role will be an umbrella European agency complementing other actors’ tasks with respect to downstream applications, focusing on creating synergies between EGNOS, Galileo, Copernicus, GOVSTACOM, and SSA programmes through transversal activities.

The ex-GSA will no longer be an agency dedicated to the EU GNSS (Galileo and EGNOS) programmes, but an agency aiming to foster synergies amongst the EU space programmes promoting the downstream/applications market development and user uptake sectors.

For the EO services community, EUSPA will focus on the enhancement of Copernicus data exploitation aiming to increase new users, new businesses and raise the competitiveness of the companies. In other words, EUSPA will be a user oriented operational agency. To do so, Fiammetta explained, their strategy is to focus more on the ‘other users’ who are researchers and non-governmental users but with a main focus on the private users while creating synergies across European space assets. Consequently, the challenge ahead is to identify the similarities and differences of the EU GNSS and Copernicus users.

Fiammetta acknowledged that although the EO and Galileo value chains are different, to achieve this goal relies on the building of a good knowledge of the user and the market. For this purpose, GSA has based this knowledge in the Galileo experience through the issuing of (six) biennial market reports[3] focused on the technology and market segments research, identifying the user communities and needs in the field of navigation. Along with this, the Horizon2020 programme has served as a key tool to develop specific products for later commercializing them.

While undertaking this market monitoring GSA has identified convergent sectors where Copernicus and Galileo have common users and sectors where these lacks of presence. For example, the transport sector is a prominent market of Galileo where Copernicus is less present, on the other hand, in the environmental sector, Copernicus is leading and Galileo lacks presence. Yet, she points out the agricultural, maritime and forestry sectors synergies are more natural to be developed.

According to Justyna Redelkiewicz, Head of Sector LBS, Market & Technology with GSA, as part of the preparatory work of EUSPA, the Agency has already prepared a ‘consolidation market monitoring report’ considering how to address the relevant markets for GNSS and Copernicus in a coherent manner. This report is planned to be released in the first quarter of 2021. Justyna mentioned several Copernicus’ market reports were used in its formulation such as EARSC reports[4], and raised a call to the industry users for input. Furthermore, Justyna mentioned that this kind of effort is important to assist the EO industry by generating accessible information on market projections.

Although Galileo and Copernicus provide different services, similarities in its users have been identified according to Eduard Escalona Zorita, Market Development Innovation Officer with European GNSS Agency. Raising awareness, however, is desired for both the Galileo and Copernicus communities sending the message that both programmes can offer a complementary solution to users. Three categories of market have been identified:

- Those sectors which are relevant for GNSS alone e.g aviation

- Those sectors which are relevant for Copernicus alone e.g climate change

- Those sectors which are important for both technologies; agriculture and urban have been cited as examples.

In this last category, synergies between the two technologies are more likely.

Finally, regarding other mechanisms, the new EUSPA encourages the industry to approach its application specialists to assist them in their business projects and also to be attentive to the incoming Horizon Europe calls to be launched this year. EUSPA acceleration programmes are also contemplated. An Entrepreneur Day will be announced very soon to assist for example in matchmaking and developing new EO ideas.

Whilst waiting for the EUSPA to take shape in its expanded role, it is clear that identifying synergies is one of its main and most challenging objectives to fulfil in this incoming era of the EU space programme. Technology readiness and users’ skills remain paramount factors to consider in order to succeed in these synergies development. EARSC has a number of projects [5] which can complement EUSPA actions and looks forward to working with EUSPA in such an integrated view of the Copernicus-Galileo future ecosystem where the user is placed in first place by focusing also on the users of the EO private sector.