Many will be following with deep anxiety the latest twist in the US after the untimely death of Ruth Bader Ginsberg. During her time as a supreme court judge, she has done more than anyone to promote people’s rights and especially those of women. If Trump is successful with his nomination of a new judge before the election, the direction of travel for these rights looks to be set back for a generation.

I write this following the most recent EARSC eocafe where the topic for discussion was “Women in Copernicus”. Nathalie Stefanne (geomatics specialist with the Wallonia public authority) is the mind behind a project to seek to give a stronger voice and visibility for the women working with Copernicus. The project, led by Marie Jagaille from GIS Bretel ( Ingénieur d'études "Applications Spatiales" et animation de projets ), aims to create a community of women (and men) to identify obstacles and opportunities for women and to provide inspiration for young girls setting out on their careers.

This is so important. As we noted during our discussion, young girls lack role models in the space sector. Whilst the EARSC secretariat is doing its best to counterbalance, if we look at the EARSC board of directors, we have 11 men and just 1 woman on the board. Is this really making best use of the skills available?

I think this is an important subject to bring the best people into positions to develop a world-class European technology and business base. In our annual survey of the European EO services sector, we find that the proportion of women in the sector is around 30% and is pretty stable at that level. We shall investigate in our next survey to see if this is changed but somehow, I doubt it. What can be done to change this?

For me, this does not mean that we should be setting targets or quotas. This does not help to develop excellence. It is a societal problem. Ruth Bader Ginsberg was clear that she was not in favour of positive discrimination when she said: “I ask no favour for my sex, all I ask of my brethren is that they take their feet off our necks”.

Our sector is not alone. Just this week, the economist published an article commenting on the appointment of a woman to be CEO of Citigroup (US banking group) bringing to 37 the number of female CEO’s at the head of the Fortune 500 companies. Also, as reported in the Guardian, the Gates Foundation has just published a report, analysing stories across six countries, saying that “Women’s voices have been “worryingly marginalised” in reporting of the coronavirus, partly due to the war-like framing of the pandemic. The Guardian article shows the extent to which men dominate the story from 100% in the UK and more than 80% in 4 of the other 5 countries.

So how to change things? Change needs to start early when girls are setting out their choices and deciding their careers. We men need to do better as well. For the eocafe, we had 54 participants of which 4 were men, and only one (Stephane Ourevitch) was from outside the EARSC secretariat! This is not good enough and is a strong indicator part of the problem; men do not see it as a problem. But that means a lot of latent talent and potential talent is not being used. If we want our sector to do better, we can start by encouraging more girls to join our industry and to make sure that they are given equal opportunity to develop within the industry.

WIC plans to launch a survey directed at the men in our sector. I hope that we can count on better male participation than last week.

I am convinced that one of the biggest hindrances to the uptake of geo-information comes from barriers within organisations. Often, we hear it described as “lack of user awareness” – which it is – but it goes deeper than that and requires considerable effort, time and patience to solve. Overcome these barriers, and the potential for the uptake of EO services becomes enormous. But how to tackle this problem is less obvious.

In our work looking at understanding and measuring the value coming from the use of EO - which goes under the name of SeBS (Sentinel Benefit Studies) - we work with key users in many different and varied organisations. For anyone who is unaware, we take a value chain approach meaning we start with a single product or service which is being used by a primary user and then analyse the impact this is having on the activities of the primary user, on the consequences for their customers/stakeholders and on the citizens of the country concerned. But having the right primary user is fundamental and tricky.

In so many cases, something goes wrong. The primary user, working with an EO service supplier, has built up knowledge and experience of how the EO service can fit into the organization’s processes. This is critical to understanding how the organization is benefiting. But what happens when the organization changes?

In around half the cases we have worked on, during the time it takes for the analysis (usually around 6 months), either the person has changed job, or the organization structure has changed meaning that our champion user has a new boss. Each time, we have to educate a new person who has none of the background or the persons themselves must educate their new hierarchy. In about one third of the cases, this leads to a blockage where the new hierarchy does not see the benefit of the analysis. The support of the hierarchy has become one of the key factors to confirm before we take on a case. Even so, it often goes wrong.

This shows clearly the problem; the use of EO is not embedded in the organization but in a few people within it. People change and the support changes. It appears that it requires a quite complex combination of skills, determination, and character to bring new technology – especially one which is not known through consumer applications – into current use in a company. It is even more difficult in public bodies which are very traditional in outlook.

I mention consumer applications and I could probably also include business applications of IT, since these are widely known if not fully understood. So, if a new IT expert advocates the use of Zoom, or even Teams, for teleconferencing, then the manager who decides is either familiar with it from home use or it is Microsoft and no-one gets fired for choosing Microsoft.

But when we come to geo-information, whilst managers may be familiar with maps, they are not familiar with maps showing lots of coloured dots designating where the ground is moving (InSAR) or of shaded areas in fields. Hence, the champion advocating for the introduction of the new technology has a much harder job, selling the solution to their internal management. Only if the benefit can be demonstrated quickly and positively can our champion convince their hierarchy that it is a useful tool for the organisation to adopt. Even then, internal politics between different departments can hinder the spread of new ideas.

This situation has been very much to the fore in some recent cases which we have analysed. One solution is to improve communication, as I wrote about recently. Another is to provide more resources to help our champion garner internal support. The SeBS case studies we believe do help in this respect by providing a story and clear evidence of the value. I should welcome any further ideas and suggestions on what more EARSC can do to help in this respect.

I have been writing these last few weeks about promoting the value in Earth Observation data, with the focus being on communicating the benefits to society at large and decision-makers. Underpinning this is another theme which I have talked about in the past which is about Capturing the Value. If you look at the value chain for communications satellites, the hardware represents about 1% with 99% of the revenue coming from downstream activities (services). The revenues for GNSS or location-based services are perhaps 10% upstream 90% downstream, whilst Earth Observation is more like 50:50.

But the value is there. In our studies into the value of Sentinels, the economic benefits being generated by the data coming from Sentinel satellites is way higher than I expected at the outset. From the 10 cases we have analysed so far, we can see benefits of perhaps €200m or more. Recent cases are showing €10m+ for each case which are based on one country. Extrapolating across Europe quickly leads to €100m+ for one application and there are literally hundreds of applications. Whilst the benefit is high, the revenue is still quite low. How do we capture more of this benefit for the sector?

This week, Joe Morrison wrote a very insightful blog The Commercial Satellite Imagery Business Model is Broken which gained traction on Twitter. Joe writes about the selling of data and the elephant in the room which is the DoD. Since the DoD are THE major customer, they are essentially setting the selling conditions. He regrets the policies adopted by major operators which makes it difficult for users like himself to get hold of data. He calls for 20% of the data to be available pro-bono for public-good use. A number of posters pointed out that the major operators already do this, but Joe’s core point that the business model for Earth Observation services is not working is largely correct. However, I don’t think it is as simple as saying the satellite operators are not setting the right conditions to sell to a mass market.

To my mind there are three forces operating here and a number of underlying issues:

- The cost of the satellite infrastructure is high. Even if newcomers with smallsats and CubeSats are pushing costs down, it is still a heavy investment and will remain so – especially for high-performance imagery and for constellations.

- There is a need for sustained data. For years, we have been launching one-off satellites (Landsat, ERS, Envisat etc) with no real continuity. Without continuity, customers are reluctant to incorporate geo-information into their business processes. With many more satellites in orbit, this has changed so that customers can be reassured that data will be available if they commit to using it. Copernicus and the Sentinels are doing this as are the commercial operators. However, assuring the data means more satellites which means more

- The lack of a sustained market. As is noted by Joe, we have been going at this for nearly 50 years now, so it is not a question of time! But it is a question of capacity and confidence that needs can be met over a period of time. Once a customer commits to using and EO product or service, they will quickly stop if they are let down by their supplier.

We see in many of the SeBS cases that much of the benefit is potential – ie it is still to be realised, which is largely because the early adopters have not yet been followed by the mass users. This is where the change is needed. We are trying to push things, through our SeBS analyses, demonstrating how the benefits are driven right along a value-chain.

So, these three forces are all interlinked. A capacity to deliver sustained data requires a very high investment which drives the costs up and makes customers hesitate to commit to a new service. The defence business is a great anchor customer, but the large benefits will come from all the host of other applications once the capacity is proven, To gain the confidence of paying customers requires more than evangelism on the part of a few enthusiasts. To generate sufficient revenue flows to justify sustained investment in upstream, observing capacity will take time. A number of enthusiastic private investors and venture funds have come into the business, but they will need to be very patient to see a return. As Joe rightly states:

“It’s a multi-decadal bet if you really believe in the power of satellite imagery to transform the commercial industries you talk about all the time.”

How do we fix this broken market? Patience and a lot of communications. In Europe, we are seeing a good number of new players coming into the value-added services markets. The data itself is becoming a commodity due to the number of competing satellite operators and the phenomenon that Joe identifies of fixing on defence customers as the motherlode. In fact, we do not see just defence in that position as governments represent 50% of the market as I have reported many times before – and I do not see this changing.

Many of the new downstream players are basing their services on the free and open data coming from the Sentinels under the Copernicus programme. With free data, it is easier to experiment without incurring high costs – as Joe points out. It is easy to get hold of through portals like the Sentinel hub. The commercial operators are also making data available free for these purposes and commercial data can also be obtained through dedicated portals for example:. https://geocento.com/

EO is not a B2C market, although I do think this can grow, so convincing the public of its value must be based on a public-good argument. Climate change could be the driver, but it could equally be global political instability post-Covid. Whichever, it is, it will take some years to develop. Investors will need to be patient I fear.

.... and thanks to Joe for kicking off a good discussion!

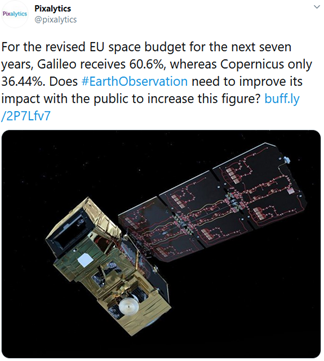

In my last blog, I raised the question of how we can ensure that our most senior decision-makers are aware of the value that EO can deliver? This theme has been picked up elsewhere and led to an interesting exchange on twitter, triggered by a blog post and tweet from Andrew Lavender of Pixalytics. Andrew had also been looking at the EU budget and wondering why Galileo was favoured over Copernicus?

Of course, as Hannes Dekeyser pointed out, there is a strategic dependence associated with Galileo that is not the same for Copernicus. Indeed, the whole Galileo programme was predicated on non-dependence – but this was at a time when there was no real global alternative to GPS. Glonass was incomplete Beidou was not even thought of. Interestingly, at that time, the UK government was opposed to the EU initiative on the basis of “GPS exists why do we need a second system?” This contrasts with the recent ambition to create the UK’s own Galileo once security signal from the EU one is to be denied them. The subsequent investment in Oneweb could be the subject of several more blog posts!

But we are interested in Copernicus and why this does not seem to leave the same impression with policy makers as Galileo. I content that this is because the general public are less aware of the benefits which satellite observations can bring. Just as the notorious US senator is quoted as saying “why do we need to invest in more weather satellites when I get thee weather every night on my television”, so the impacts of Copernicus are much more felt by businesses and by other government departments than by those taking spending decisions. Governments rely so much on focus groups to gather public opinion, and the general public is unaware. Whilst they have satnav in their cars and in their phones, there are very few EO applications which touch the citizens. Hence they remain unaware of the benefits and the public decision makers reflect their views.

Again, going back to Galileo. In the early days, when the debate over the programme was raging (this is 2001/2002), it was easy to engage a taxi driver in a discussion. What is this Galileo I keep hearing about on the radio? It is a European GPS. Oh well then it is a good idea. But, asked if they know of GMES (or Copernicus), there is no similar answer.

The conclusion is that we need to do much more to raise awareness of the impact EO and Copernicus has on everyone’s lives. Climate change gives us a good angle but our SeBS studies provide plenty more ammunition. I like Steven Krekels proposal concerning natural capital accounting. With so m much more awareness around environmental impact arising from the Covid pandemic, it is a good time to be raising awareness of the essential role played by satellites. The new CO2 monitoring mission will help grab attention but we cannot wait and need to promote the impact our technology has on everyday lives. It is true as Bert Rijk says that we have been going at this for 50 years, but this has been 50 years of science. Only now is the technology becoming mature to make a strong impact. Again, many of our SeBS cases show this very well. See the recent one on Norway where the benefit of the use of InSAR to help manage roads, rockslides and many other problems faced by Norwegian society is so clear – yet is only just starting to be appreciated. This is the same in many other countries and for many other issues of national interest.

I am sure we can develop a strong campaign. It is a personal target to contribute to this debate and to help develop both content and communications to deliver the messages. We are encouraging a community of interest called GeoValue with this particular goal and I look forward to working on this with yourselves and others on behalf of the sector.

The recent announcement of cuts in the EU budget for the space programme discussed in my last blog, came at a critical time and indicates the pressure which EU leaders were under at the time. I expressed our disappointment at seeing a significant cut in the budget for Copernicus that amounted to nearly 20% from initial proposals (€6b down to €4.8b). It is likely that one of the new Sentinel missions will need to be cancelled or postponed.

But, as leaders cut the space budget, are they aware of the benefits which the investment brings? Overall, the impression is that leaders and governments in general are not aware and treat the space budget as a strategic investment securing a place on the geopolitical stage ie Europe’s place in the world. Historically, the investment in the civilian space effort has been considered as a part of the R&D activities.

But the EARSC survey into the EO services industry shows that over 50% of the public sector spend is as a user of EO satellite data. This number has been consistent since we started the survey back in 2012 – and has even grown slightly over that period. This demonstrates that the use of the EO data by public sector decision makers is operational and supports public sector efforts.

But these users are not those investing in the space programme. They are in charge of other policies and public programmes and so they do not see the link between what they do and the investments made in space and in Copernicus. If they do see it, they see the size of the space programme as being too significant for them to support by themselves. I recall this very clearly in the very early days of GMES when we were trying to get DG Environment (DG-XI at the time) to support the proposal. DG Environment had to be told, and reassured, that they were not being asked to pay – but their support as a key user was necessary to move the proposals along.

These roles are many and varied ranging from understanding and combatting climate change, to supporting regulation, the building of roads, the move towards digital farming, the supply of essential goods through ice-bound waters etc etc. All these examples can be found within our work on demonstrating the value in EO through the programme we call SeBS (Sentinel Benefits Studies).

Indeed, the SeBS cases show that enormous value is being delivered which underpin and more than justify the investment by each European country in the Sentinels and Copernicus.

So, how do we ensure that our most senior decision makers are aware of this value?

More effort is necessary to communicate and more effort is needed to construct the case. In SeBS, we believe we have developed a robust methodology which can be used by anyone. We are working with other international partners under the umbrella of GeoValue to share our knowledge, to learn from others and investigate how to extend the methodology further. With ESA, under SeBS activities, we develop stories of how the cases work. Each case demonstrates value on its own but in combination we are able to obtain a truly rich perspective on how EO is delivering value to decision makers whether they are in the public or private sectors.

We also put effort into communicating the benefits, but it is clear that more is needed. We need to reach the most senior decision makers with this key message. Our work will come under more scrutiny, but we are happy to help others and to learn ourselves if we can improve our methodology further. Mostly, we seek help from our members and partners to spread the word and to inform us if there are new cases or specific topics which can hit home. Let’s work together to

The meeting of the EU Council has proven a marathon affair extending into the 5th day of meetings – including 4 full nights. The agreement reached (see the council conclusions), despite the denial of the term by Mark Rutte the Netherlands prime minister, is certainly historic. For the first time, EU nations have agreed to pool debt to help out those most affected by the Covid-19 crisis. That was never going to be easy.

The new budget of €1.8t includes the famous €750b dedicated to Next Generation EU (NGEU) and comprises a mix of grants and loans – for which negotiation over the balance and conditions attached caused the 4 sleepless nights. A small amount of this budget is attached to climate related activities in the Just Transition fund of €10b.

The second part of the budget of €1,074t is the MFF for 2021 to 2027. This includes all the traditional EC funded activities including Horizon Europe and the Space programme. Here, in some key areas of much interest to the EO services community, the news is not so positive.

The much-awaited EU space budget – the first time that a specific budget has been allocated to a programme of space activities – has been cut as a result of the negotiations. Originally sized at €16.1b by the EC proposals, and resized to €14,8b before the summit, the proposal which emerges is for a budget of €13,202m of which €8,000m is for Galileo and €4,810m is for Copernicus.

"........will continue to support funding to large scale projects in the new European Space programme as well as to the International Thermonuclear Experimental Reactor project (ITER): i.The financial envelope for the implementation of ITER for the period 2021-2027 will be a maximum of EUR 5 000 million. ii.The financial envelope for the implementation of the Space programme for the period 2021-2027 will be a maximum of EUR 13 202 million, of which EUR 8 000 million will be dedicated to Galileo and EUR 4 810 million to Copernicus."

Another area to be cut is the budget for Horizon Europe; from an initial proposal of €100b only €75.9b will be allocated. Some of this cut is not a surprise given the absence of the UK and we wait to see how UK wishes to associate to the European research programme, but it still represents a severe cut and another major disappointment.

Another disappointment given the Covid crisis is the cut in budget for health. The EP had been proposing a €9b fund for common procurement of PPE, vaccine research and other measures. But EU leaders did not wish to cede these competencies and have cut the budget to €1.7b. It could be considered a small step forward but given the news of the EU response to an Italian request for help early in the crisis, more might have been realistically expected. Maybe some other budgets hide measures which will emerge in time.

For space and EO, it is a disappointment that the core budget for Copernicus should be cut so drastically. Here also, maybe other budgets will be relevant especially environment, agriculture and climate change, and the Council has maintained the emphasis on fighting climate change.

"Reflecting the importance of tackling climate change in line with the Union's commitments to implement the Paris Agreement and the United Nations Sustainable Development Goals, programmes and instruments should contribute to mainstream climate actions and to the achievement of an overall target of at least 30% of the total amount of Union budget and NGEU expenditures supporting climate objectives. EU expenditure should be consistent with Paris Agreement objectives and the "do no harm" principle of the European Green Deal. An effective methodology for monitoring climate-spending and its performance, including reporting and relevant measures in case of insufficient progress, should ensure that the next MFF as a whole contributes to the implementation of the Paris Agreement."

It will be more important than ever to show, concretely, the value that our industry brings to Europe and the enormous benefits which may be secured through the use of EO-based information and services. We should rightly emerge not as “a space industry” but as part of the information sector working with satellite data.

The dust now needs to settle. The EP will have its’ say next but given the fragility of the agreement and the difficulty of reaching it, further change seems unlikely. Despite the disappointments, the deal is extremely important for Europe and without it, the EU would have been under even stronger pressures and possible leading to even larger disruptions to which even Brexit might have seemed soft by comparison.

Our Annual Meeting took place last week on 18th June. My colleague Delphine Miramont has written a short overview of the proceedings. It is our plan to establish a new blog over the summer where my (Geoff's blog) will move and sit alongside other blogs including a policy blog which will allow Delphine to write about relevant happenings in Brussels. Until that blogpage is ready, we'll introduce her blogs into my blog here. If you want any more information, do not hesitate to leave a comment here for her to reply to.

Policy blog by Delphine Miramont

AGM – 18th June 2020

On the 18th of June 2020, EARSC organised its annual conference, gathering Earth Observation industry members and key European stakeholders, namely Mr Massimiliano Salini (representing the European Parliament), Mr Josef Aschbacher (European Space Agency), Ms Paraskevi Papantoniou (European Commission, DG DEFIS), Mr Kai-Uwe Schrogl (German presidency of the European Council) and Mr Chetan Pradhan (Chairman of EARSC).

The on-line event was very successful giving a comprehensive overview of the future of the European Space programme. Against the background of the Covid crisis, the guest speakers expressed their views and concerns regarding the governance and the budget of the European Space programme.

- Industrial competitiveness and the EU Space programme: a holistic approach

Mr Salini, who was appointed rapporteur of the EU Space programme in 2018 by the ITRE Committee strongly believes that industrial competitiveness is key to a Europeanand digital strategy. Mr Aschbacher shared this holistic approach and regretted that the budget for the space programme would not cover all the proposed missions. Both speakers pleaded for a strong push for an industrial strategy at the European level, in which the EU space programme is a key element. As for the European Commission, Ms Papantoniou stressed the role of the member states in the governance of the post Covid-19 context and the importance of programmes such as Horizon 2020 to provide a strategic autonomy for Europe and boost innovation and resilience. She added that the priority is to federate more the European players to foster entrepreneurship.

- Impact of Covid-19

Of course, the consequences of the Covid 19 crisis on the industry was one of the main topics discussed during our workshop. EARSC recently conducted a survey to measure the consequences of the pandemic crisis on the industry and the first results show a negative impact on the business in the mid and long term. In that regard, Mr Salini mentioned a letter[1] that he wrote to Thierry Breton, asking for a recovery plan for the space industry. explained that the coronavirus pandemic makes it more crucial for the European Union to commit to the €16b funding level which had been proposed in the context of the MFF compared to €14.9b in the revised plan. A letter[2] from EARSC to Commissioner Breton also highlighted the necessity of sustained funding to support the recovery of companies. At the ESA level, Mr Aschbacher also talked about the different support measures taken to help the industry (advances payments, faster processes…).

- Copernicus programme

Mr Aschbacher reinforced the position of the Copernicus programme and strongly asserted that the Copernicus data and services will be helpful for the Green Deal and the digital strategy. He also mentioned the necessity for the industry to be prepared for the next phase of the programme. This statement is aligned with EARSC last position paper concerning the evolution of the Copernicus programme and the need to prepare in a timely manner for the Copernicus new services.

[1] Letter to the Commissioner Thierry Breton, Bruxelles, Massimiliano Salini MEP, Carlos Zorrinho MEP, Christophe Grudler MEP, Andrea Caroppo MEP, Damian Boeselager MEP, Evžen Tošenovský MEP,

Manuel Bompard MEP, 30/04/2020,

[2] Letter to the Commissioner Thierry Breton, EARSC, Bruxelles, 09/04/2020.

Recently, I read with interest that the US Department of Commerce has published proposals for revision to the export limitations for EO satellites and data supplied by US companies. The original restrictions were part of the Landsat Remote Sensing Policy act published way back in 1992. This was revised in 2006 in part reflecting the Commercial Remote Sensing act of 2003. Now the DoC wishes to remove many of the constraints which have been barriers for US companies in the global market.

The market has changed significantly since the last review (to put it mildly!). In 2006, public systems still dominated completely the EO satellite ecosystem. Since then, the launch of many systems by private companies has transformed the market so that data which a few years ago would only be available to military users, can now be accessed relatively easily. In consequence, the DoC is responding to pressure from the US industry to remove the barriers and enable them to compete more effectively in the market outside the US.

The emphasis has moved from direct control over who can have what data based on national security considerations to ensuring that the US has the capacity through an industry competing in the world market. This brings it much more in line with European policy which has relied for many years on its industry maintaining its competitiveness through export business. The revenue for EU space companies have been around 50% commercial and 50% governmental for many years whereas for the US the figure is closer to 20:80 for a much larger business underpinned by DoD budgets.

Now the US seek to move more towards the Europen model. As the DoC sees it:

Through the National Space Council, this Administration recognizes that long-term U.S. national security and foreign policy interests are best served by ensuring that U.S. industry continues to lead the rapidly maturing and highly competitive private space-based remote sensing market. Towards that end, the Administration seeks to establish a regulatory approach that ensures the United States remains the “flag of choice” for operators of private remote sensing space systems.

The regulation shifts the process away from a control based on security factors to one which more reflects international competition. If a specific type of data is available from other sources (US or non-US) then the company seeking to sell its data will automatically be able to do so. The system is more transparent and much more flexible.

In consequence, European companies, which are currently leaders in the market, will face increasing competition from US players. The more favourable and more easily accessed sources of financing in the US, will also act to encourage non-USA companies to incorporate in the US.

What should Europe do?

The regulatory environment in Europe is very different to the US. Defence is a national competence and European nations have their own approaches to control. This has led to some restrictions for very high-resolution systems but nothing like the same barriers as have existed in the US. As a result, European companies have had a much easier ride when exporting either satellite systems or data.

Just as the US is removing controls, Europe does not need to impose them as was being considered by the EC a few years ago. Rather, other steps will be necessary to enable the European industry to maintain its edge. For, whilst the new measures will help US companies to sell data and services elsewhere, it does nothing to open up the US market to non-US suppliers. Here there is still work to be done.

In our recent position paper, we (EARSC) set out a number of measures which we hope the European Union will be able to implement. I wrote recently about innovation and how small measures can bring large rewards by linking industrial policy to other policy measures. I was explicitly referring to Copernicus where public needs can be met by private suppliers and in doing so, can open up business opportunities for European suppliers. The public sector can encourage companies to invest in innovative products and services by setting out its service needs and leaving the private sector to compete. The policy tool of anchor tenancy is a powerful one which can be even further developed by using pre-competitive procurement to stimulate innovative solutions. Overall, we seek to closely align industrial policy with other policies.

Our proposals were sent to Commissioner Breton - who is in charge of the DG Defence Industry and Space (DEFIS) - along with a letter setting out our supplementary views on the impact of the Covid crisis. Both can be found in the website library and we await with great interest to see how the Commissioner will respond to our suggestions.

I was asked yesterday if I thought that the public sector is doing enough to promote innovation (in industry)? I was participating in a workshop (on-line of course) looking at the results of a survey into SME’s in the GI sector. The survey had been conducted by the JRC and the on-line workshop replaced the physical one which had been planned for early April.

It was very enjoyable and left me regretting that we had not been able to meet and certainly have some really interesting discussions. The time available to exchange on-line and the singular nature of the exchanges means that topics are not developed as far as they might otherwise be. This was very much the case here where I really wanted to challenge some of the views and enter into more discussion. Others would almost certainly also have wished to challenge me!

The initial response to the question I posed above was that this is not the role of the government. Rather, the public sector is an important customer for geospatial services, and it is for the company to develop innovative solutions which then become a source of competitive advantage. Now of course, to an extent, this is true. An operational public department, maybe part of a local authority, has a limited budget and is only (rightly) concerned with results. But for me, this is a bit too simple.

In our (EARSC) survey of the industry, we find that the public sector generates around 65% of the revenues of the EO services sector. The JRC SME survey finds roughly the same for geospatial services. But this disguises an important and key fact. Some 50% of the revenue is coming from the public sector as a customer whilst 15% is coming from R&D or industrial policy activities. In other words, nearly 80% of the spend by the public sector is for services which they need for their public mission. We can go further because some of the R&D expenditure is to improve the services which they are themselves buying. So, of the 65% of sector revenues, around 85% is needed by the public sector.

The key point here is to distinguish between the role of the public sector as a customer and that as a sponsor. Indeed, the public sector confuse these roles themselves as may be seen in the organisation of the European Commission itself! Copernicus is a space programme coming under the DG for Defence Industry and Space. How much better and clearer if it came under a DG with responsibility for geospatial information – together with a geospatial agency to deal with operational aspects.

Returning to the question. As a customer, the public sector may not be directly concerned with stimulating innovation which is more directly linked with research ie Research and Innovation. But why not link the policies to get the maximum benefit from the public investments? In this way, customers in the public sector can stimulate innovation in industry (and academia) to help create a more competent industry with the capacity to compete in the global market. A mechanism does exist for this, but we should seek others as well. The existing mechanism is called pre-competitive procurement which is a policy which originates in the US, has been used in Europe but not enough in my opinion.

So, in answer to the question, yes, I think the public sector should and can do more to drive innovation in industry and by doing so improve the services which they make use of at the same time as helping the industry develop its own competence to compete in world markets. At this time of recovery from the Covid crisis, this can be an excellent tool to help rebuild industry.

I wrote previously about the Covid situation in Italy and some thoughts on how the situation might be brought back under control. Now one month later, many countries in Europe are starting to unwind slowly the confinement measure imposed – absolutely necessary in my view – to bring the pandemic under control. Some countries seem to have used the time to prepare for a test, trace and isolate system to maintain control whilst others such as UK and USA seem only to have been concerned with communications rather than a serious attempt to reduce the impact on their countries.

In Belgium, I believe the authorities are doing a good job. They are very transparent with the figures and how they are calculated and the only issue which concerns me is that the capacity for testing could be higher. The appropriate response to the pandemic has changed and with the system in place, no longer are national figures relevant and we should be looking for small local outbreaks which, like small fires smouldering after a major incendiary, need to be snuffed out quickly before they can take hold.

We have been conducting a survey of our members to see what impact the pandemic is having on them. The results show that most companies have adapted quite well to the situation by moving their production out of the offices and into employees homes and that few are suffering immediate problems. Most of their revenues are coming from contracts (rather than single product sales), most can be executed on-line and some are even seeing advantages coming from the shut-down. For example, it is much easier to fly survey aircraft at this time. There is also demand for information on natural resources and statistics linked to the pandemic.

However, most are somewhat fearful for the future in 6 months when contracts start to come to an end and customers budgets are squeezed due to many competing priorities. The first concern is for commercial contracts where private-sector customers will face cash-flow issues but public budgets will also be affected. In my view, they may also face problems with access to capital, as lending will be in heavy demand and competition fierce.

But with a crisis come opportunities and the EO services sector would appear to be in a position to benefit as well. The much-heightened awareness of security of supply chains will generate a need for more business intelligence to inform on bottle-necks, on delivery channels, and on capacity. The links between the crisis and environmental factors will increase the demand both for climate-related information and specific environmental / ecosystem factors such as deforestation, sustainability, pollution risk etc. And of course, the climate pressures, although ameliorated slightly in the short-term, will not go away and the need for more information linked to security and threats from natural disasters is likely to accelerate.

And a final thought, the crisis is going to drive significant M&A activity as companies with cash and buying power are able to seek out bargains. Will we see a wave of consolidations in the EO and space sectors?

At EARSC, we seek to help companies prepare for this changing world, firstly by surviving and secondly to offer the best products and services to as large a market as possible. We shall continue to do this. At the end of next month, I shall hand the role of secretary-general over to my successor – Emmanuel Pajot. I shall continue to support EARSC but just at a lower level of activity than at present. I’ll no doubt write about this again in the future. In the meantime, stay safe.

China today reports no new cases. How did they manage to gain control over the virus to this extent? I came across this interview which explains how it was done. Basically, it involves testing, testing and more testing as we have already heard but crucially, the first test is to take the temperature and any anomaly is immediately isolated. No home quarantine since the first group to get infected is the family. So, anyone with a temperature was obliged to go to a fever clinic where they are tested further. Firstly, with a blood test to see their white cell count, which, if normal means no viral infection and they can go home. Secondly a test for the normal flu (if positive then they can go home) and then through a CT scan to detect any lung damage. If none is found, then again, they can go home. Only if that is positive, are they tested for the Coronavirus and if that is positive, then off they go to a quarantine centre to see how their illness will develop. These are the new hospitals which we saw being built in 8 days in Wuhan.

To support this, every person is required to self-test every day and to report the result and is tested whenever they go out and move around. This is backed up by the district manager who appears to play a crucial role in the process. Responsible for a district of about 1000 people, the district managers are close enough to each of them to know what they are doing. They are informed of the temperature of each person every day and of course know if people are breaking the quarantine in any way. These strict social controls seem to have been the key in China; would this be acceptable in Europe?

The key question is what measures are really necessary to control the spread of the virus? Is a complete confinement necessary? What degree of social distancing is effective? How free will our society be once the cases have stabilised? How many cases per 1000 people per week is an acceptable number? And on a more sinister note, what form of society will emerge from this whole pandemic?

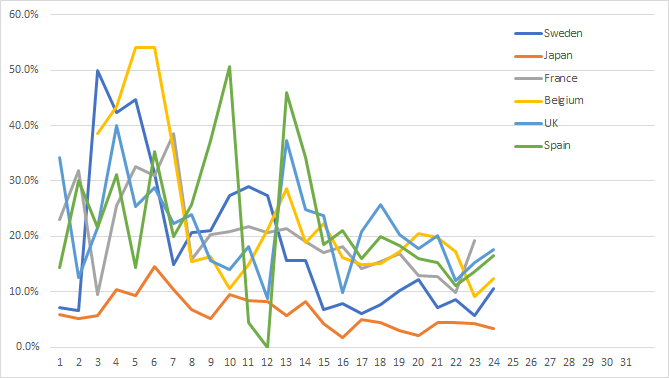

I wrote 1 week ago about the situation and I included some of the curves which I have been tracking each day. There are many others doing the same thing, but I do not see them being talked about very much, even if they are key to understanding the situation – and knowing what to do later. One of the interesting factors is how the situation has evolved in different countries each taking different measures and reflecting underlying societal differences. I talk about China above, but South Korea has managed a measure of control without such drastic measures (through extensive testing and tracing of contacts) and Japan is a complete anomaly which experts are starting to try to understand.

It is important to understand that in this analysis it is not the absolute numbers which are critical as these depend on the test regime in place and many local conditions. But assuming that a country or region follows the same regime from day to day, the rate of change is the critical factor. Last week I posted the charts for Northern Italy and Lombardy. I am following 3 of the provinces which were locked down on 28th February and 2 which were locked down with the rest of Lombardy on 8th March. These are all trending downwards which looks as though the peak of new cases has passed and some control has been achieved.

Note this is a long way from being an acceptable rate. The number of deaths will still rise, lagging the number of new cases by up to 14 days – this is already destined. But if the rate comes down then it shows the measures are working.

No other European country (with the exceptions of Sweden and Denmark) is yet showing such a response and the daily cases continue to grow at rates between 10% and 20%. Germany seems to be one of the better ones whilst Sweden is lower despite not having a confinement strategy. Maybe these will be guides for the future although the Swedish government is coming under criticism for not doing more.

Happy to exchange views with people and I hope that I am not adding to your Coronavirus information overload in writing this short note.

So, as of today, in Belgium, as in France and many other countries in Europe, we are now officially confined to our homes. The temptation to go out has been removed by closing bars, restaurants and most shops. Fortunately, it seems that we are still allowed to go to the park to walk our dog as long as we don’t meet and socialise with any of the other dog walkers doing the same thing. This has to be the right policy at the moment as the first priority must be to bring the epidemic under control. Only then can we start to see what level of social interaction will be possible afterwards. There seems little doubt that we are in this for the long haul.

It is now widely understood that the goal of the measures is to bring the level of infections down to a point where they can be managed by the health services. To understand that we need to look to China and Korea which have managed to achieve control and the rate of infections has slowed to a manageable level. Testing, testing and more testing is their advice, echoed by the WHO.

How long can we expect it to take to bring under control? It seems to have taken about 4 weeks in both China and Korea. In China, a total shut-down in Hubei (around Wuhan) was imposed; measures which would be difficult to impose in Europe. In Korea, the response was less rigid, but the outbreak started in a religious group which allowed better tracing of contacts; contact tracing is one of the key tools to control the spread. In both these countries the rate of new infections has fallen to a very low level. Can this be maintained is the key question?

But how is Europe doing? Italy was the unlucky precursor where an outbreak happened in Lombardy (starting in Codogno in the province of Lodi). On 28th February, a lock-down was imposed around Lodi (then extended to Lombardy (8th March) and then around the whole country (10th March). Other countries have followed.

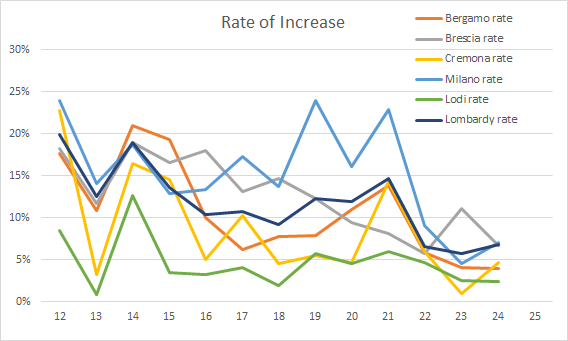

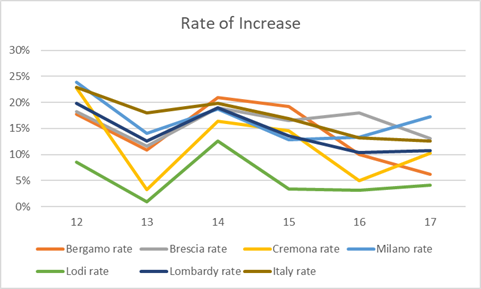

I have been keeping watch on the rise of the epidemic and in particular watching the rate of cases in key regions; Lodi, Lombardy and Italy. They may be interesting for others. I am writing on the 17th March, so figures are from yesterday and it is looking as though the number of cases is starting to fall. Fingers crossed that this really is the case. The new cases in Lodi have been around 40 per day compared to 140 3 days ago and around 80 before that. For Lombardy, the rate has fallen for 2 days in a row and the most recent figure for the whole of Italy is lower than the peak.

I am just making very simple analyses but using original data. Several sites are really helpful to keep track:

Wikipedia: https://en.wikipedia.org/wiki/2019%E2%80%9320_coronavirus_pandemic

An analysis by a data scientist, Mark Handley at UCL London. http://nrg.cs.ucl.ac.uk/mjh/covid19/

The second is particularly insightful as it is trying to rebase all the countries curves allowing for the differing conditions at the outset. The general rate of increase has been 35% (doubling of cases every 2.5 days) but this is falling to 22% and lower where measures have been taken (Italy overall is standing at around 11%). There is also evidence to suggest that the rate is different between warm and colder countries. But none of these have been showing the Lodi numbers which in theory should give the earliest counter-indication (these are sourced from the Italian Ministry website:

http://opendatadpc.maps.arcgis.com/apps/opsdashboard/index.html#/b0c68bce2cce478eaac82fe38d4138b1.

The Italian numbers are published each day at 6pm and, below, I give the current propagation rates for the key provinces in Lombardy. Lodi has fallen below 5% whilst Bergamo is falling rapidly and the overall trend is down as it should be. What is an acceptable level of increase? As a maximum it should be less than the recovery rate which I shall start to look at.

This is only the start, but it is essential to bring this thing under control or risk many more deaths than need be the case. We need to keep a watch on China and Korea to see if they can avoid a 2nd wave, and on Italy to see how fast a measure of control can be achieved under western conditions. After that, we may need to see regular bouts of social distancing until 60 or 70% of the population has been infected or a vaccine has been developed. Let us hope that the 2nd comes first.

Warning: I have no competence in epidemiology or in medicine in any way. I am simply reading, playing with some numbers and drawing what are possibly flawed conclusions. I am happy to receive comments and to exchange further on the subject for anyone interested.

As I reported in my last blogpost, EARSC staff are all still working; all from home and not all full time as arrangements are made with partners and especially with children. For the moment at least we can carry on almost as usual and facing many challenges to organise remote events. I am sure it is the same for our members. We should be happy to hear from you and we’ll continue to report here.

Good luck to everyone. We are all in this together.

You have probably seen that the Belgian Federal government decided last night to take some stringent measures to prevent the development of the CoVid-19 virus in Belgium. These included the closure of all schools, cafe's and restaurants and the limited opening of shops up until 3rd April.

The EC has also now decided that all staff should work from home and there will be no visitors.

As far as EARSC is concerned we in the secretariat are all affected by these measures in different ways and each member of the secretariat is adapting their way of working according to their specific situation. Those with children are most impacted.

However, for the moment at least, EARSC will continue to work normally - albeit with significant teleworking. We are working on projects and services where we can work remotely and continue to make progress - and are doing so. Some of our activities are directly concerned; most specifically for PARSEC where a Bootcamp was to have been organised at the end of March. With the agreement of the EC (as it is a contractual requirement) this was changed last week to being a virtual bootcamp and our team are exploring how best to manage this very great challenge to organise a virtual matchmaking type event. It is going to be very interesting to see how this works.

Another large project for us at the moment is preparing our annual conference ExpandEO. For the moment we are committed to going ahead towards the end of June, but no-one can say what the situation will then be and we shall certainly inform you of any change to this.

For other projects, we are working on certain deliverables and awaiting further legal information regarding the contractual obligations. We already know that incurred costs will be covered in the event of cancellation but for new events we are still uncertain.

Please contact us with questions if you wish and we shall keep you informed as usual through our monthly report, through our blog, through social media channels (@EARSC) and through any news on our website (www.earsc.org/) and our portal (earsc-portal.eu).

The situation will be reviewed on a daily basis and we shall inform you of any changes which may affect the service which we provide you with.

On behalf of all the EARSC team, I wish you strength to carry through this exceptional crisis and hope that you all emerge the other side with as little damage as possible.

As we start the new decade, a number of topics are stimulating the discussions in the space community and in Brussels. One of the first events of each year is the space policy conference in Brussels; this years’ is the 12th. One word is dominating the sessions’: defence. I noted last year that this topic was rapidly rising up the European Union agenda. This year it is not just spoken but is also written into titles of sessions and the topics from many speakers. It is of course reflected in the new Commission organisation which for the very first time has a Directorate-General (equivalent to a ministry) with space in the title and with defence as well.

The new DG-DEFIS, for Defence Industry and Space, is just taking shape. The director-general is Timo Pesonen (Finnish) working under the Commissioner for the Internal Market, Thierry Breton. Changes to the organigramme have been announced and the set-up starts to take shape. The change has certainly led to a hiatus, to a period with a lot of uncertainty. This should all be dissipated as the new structure finds its feet.

The other major topic of the conference reflects a priority for the new Commission, the Green Deal. Space and Earth Observation will be a significant contributor to implementing the Green Deal and we shall devote a lot of effort to ensure that the contribution that EO services can make is recognised and integrated wherever needed. We are working on a new position paper looking at the next phase of Copernicus and I am sure this will feature quite strongly even if, at the moment, space does not feature strongly in the Green Deal documents.

Just before the Christmas, the ESA ministerial held in Seville, led to a record budget for ESA voted by its member states. The support for ESA investment into the Copernicus programme through the development of new Sentinel satellites was over-subscribed indicating very good support from Member States for Copernicus as well as the overall space programme. Hence it was a surprise when the EU council voted to reduce the budget for the space programme under the next Financial Framework.

For those less familiar with the set-up in Europe, the ESA budget will pay for the technology development of new satellites and sensors, whilst the EU budget pays for the operational spacecraft, part of the ground segment, data from the contributing missions and the services. Everyone has been taken by surprise by the unexpected decision to cut the EU budget by 20% but we shall follow the evolution very closely and intervene where we can put the arguments why this budget should be restored to its full level.

EARSC has also started the year well. The Board of Directors met on 22nd/23rd which included meetings with 3 important guests. Carlo Des Dorides who heads up the GSA (Global GNSS satellite systems Agency) which will become the EU Space Programmes Agency on 1st January 2021, spoke about how the agency will evolve to embrace some responsibility for the market develop for Copernicus and the positive relationship he sees with EARSC in the future. Josef Aschbacher, Director of Earth Observations at ESA spoke about his plans following the very successful ESA Ministerial, whilst Philippe Brunet, Principal advisor at DG International Development explained his new role and what it could mean.

I write this before the Chinese new year and so it leaves me open to wish everyone a Happy, healthy and successful 2020 and I hope to see many of you in various events throughout the year (you can follow on this blog and our website).

The ESA Council of Ministers meets this week in Seville to approve the programme plans of ESA and especially the budget allocations. EARSC has issued a statement supporting the ESA proposals and especially those linked to Future EO, Copernicus 4.0, In-cubed+ and for Global Development Assistance. These are all very important for our sector.

Studies have shown that for every €1 invested through ESA, a return of €3.8 is generated for the Member State. But for Copernicus, the benefit is a great deal higher as government is not only a sponsor but also a key user of the products and services which are generated. As a result, this benefit rises to €10 in socio-economic for European society in return for every €1 invested.

The EO services sector is crucial to delivering these returns. This is illustrated through 2 studies which EARSC has conducted and is conducting. The first looks at the European EO Services industry sector through our biennial survey of the industry. The industry comprises over 515 companies throughout Europe, with 8,400 employees delivering over €1.2b of revenue. The sector is growing at a rate of 10% per annum. The report is available on our web-site.

In this we find that the government sector makes up 65% of the revenue base for the sector. Of this 15% is for R&D actions and 50% represents government buying services to meet its own needs. Now maybe up to half of the R&D spend will also be in support for meeting government needs so we can safely say that more than 50% of the market is to meet government geospatial needs – ie government as a user. It also means that government provides around 10% of the total sector revenue as a sponsor for the sector. It is highly important to clearly distinguish these two roles.

In the study - SeBS; Sentinel Benefits Study - we work to analyse cases where Sentinel data is being used operationally to deliver benefits to a whole value chain; at the head of which is what we refer to as the Primary User. Our approach is to look at the use of a single product or service by this primary user and how that impacts along a value-chain. We have looked in detail at 8 cases so far which show a combined socio-economic benefit of over €200m per annum. But, in most of these the full potential has not yet been reached and both market and technology development will increase the use and value of the services. For these 8, we can identify a minimum potential of an additional €100m.

Furthermore, each case is based on one country and by extending the service to other countries, the benefits will grow significantly. We do not yet have enough evidence to support the further geographical extrapolation but it does seem to more than support the 10:1 benefit ratio given at the outset and can most likely justify an even higher figure.

As we analyse more cases, we plan to address the question of extrapolation and we shall also extend the consideration of benefits to other dimensions such as better regulation, innovation and entrepreneurship creating new jobs and the contribution to scientific advancement. These will go along with the socio-economic benefits and also the socio-environmental ones.

The European EO services industry works alongside ESA to exploit the investments made in the upstream sector. The subsequent downstream benefits are significant, and we really encourage ESA ministers to support the ESA investment plans and agree the new programme proposals to be tabled in Seville. The stakes are high to maintain a European lead in the sector but then the return on investment to Europe is very high.