I have been writing these last few weeks about promoting the value in Earth Observation data, with the focus being on communicating the benefits to society at large and decision-makers. Underpinning this is another theme which I have talked about in the past which is about Capturing the Value. If you look at the value chain for communications satellites, the hardware represents about 1% with 99% of the revenue coming from downstream activities (services). The revenues for GNSS or location-based services are perhaps 10% upstream 90% downstream, whilst Earth Observation is more like 50:50.

But the value is there. In our studies into the value of Sentinels, the economic benefits being generated by the data coming from Sentinel satellites is way higher than I expected at the outset. From the 10 cases we have analysed so far, we can see benefits of perhaps €200m or more. Recent cases are showing €10m+ for each case which are based on one country. Extrapolating across Europe quickly leads to €100m+ for one application and there are literally hundreds of applications. Whilst the benefit is high, the revenue is still quite low. How do we capture more of this benefit for the sector?

This week, Joe Morrison wrote a very insightful blog The Commercial Satellite Imagery Business Model is Broken which gained traction on Twitter. Joe writes about the selling of data and the elephant in the room which is the DoD. Since the DoD are THE major customer, they are essentially setting the selling conditions. He regrets the policies adopted by major operators which makes it difficult for users like himself to get hold of data. He calls for 20% of the data to be available pro-bono for public-good use. A number of posters pointed out that the major operators already do this, but Joe’s core point that the business model for Earth Observation services is not working is largely correct. However, I don’t think it is as simple as saying the satellite operators are not setting the right conditions to sell to a mass market.

To my mind there are three forces operating here and a number of underlying issues:

- The cost of the satellite infrastructure is high. Even if newcomers with smallsats and CubeSats are pushing costs down, it is still a heavy investment and will remain so – especially for high-performance imagery and for constellations.

- There is a need for sustained data. For years, we have been launching one-off satellites (Landsat, ERS, Envisat etc) with no real continuity. Without continuity, customers are reluctant to incorporate geo-information into their business processes. With many more satellites in orbit, this has changed so that customers can be reassured that data will be available if they commit to using it. Copernicus and the Sentinels are doing this as are the commercial operators. However, assuring the data means more satellites which means more

- The lack of a sustained market. As is noted by Joe, we have been going at this for nearly 50 years now, so it is not a question of time! But it is a question of capacity and confidence that needs can be met over a period of time. Once a customer commits to using and EO product or service, they will quickly stop if they are let down by their supplier.

We see in many of the SeBS cases that much of the benefit is potential – ie it is still to be realised, which is largely because the early adopters have not yet been followed by the mass users. This is where the change is needed. We are trying to push things, through our SeBS analyses, demonstrating how the benefits are driven right along a value-chain.

So, these three forces are all interlinked. A capacity to deliver sustained data requires a very high investment which drives the costs up and makes customers hesitate to commit to a new service. The defence business is a great anchor customer, but the large benefits will come from all the host of other applications once the capacity is proven, To gain the confidence of paying customers requires more than evangelism on the part of a few enthusiasts. To generate sufficient revenue flows to justify sustained investment in upstream, observing capacity will take time. A number of enthusiastic private investors and venture funds have come into the business, but they will need to be very patient to see a return. As Joe rightly states:

“It’s a multi-decadal bet if you really believe in the power of satellite imagery to transform the commercial industries you talk about all the time.”

How do we fix this broken market? Patience and a lot of communications. In Europe, we are seeing a good number of new players coming into the value-added services markets. The data itself is becoming a commodity due to the number of competing satellite operators and the phenomenon that Joe identifies of fixing on defence customers as the motherlode. In fact, we do not see just defence in that position as governments represent 50% of the market as I have reported many times before – and I do not see this changing.

Many of the new downstream players are basing their services on the free and open data coming from the Sentinels under the Copernicus programme. With free data, it is easier to experiment without incurring high costs – as Joe points out. It is easy to get hold of through portals like the Sentinel hub. The commercial operators are also making data available free for these purposes and commercial data can also be obtained through dedicated portals for example:. https://geocento.com/

EO is not a B2C market, although I do think this can grow, so convincing the public of its value must be based on a public-good argument. Climate change could be the driver, but it could equally be global political instability post-Covid. Whichever, it is, it will take some years to develop. Investors will need to be patient I fear.

.... and thanks to Joe for kicking off a good discussion!

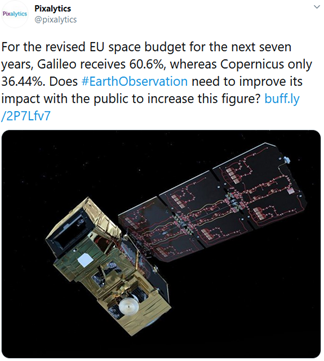

In my last blog, I raised the question of how we can ensure that our most senior decision-makers are aware of the value that EO can deliver? This theme has been picked up elsewhere and led to an interesting exchange on twitter, triggered by a blog post and tweet from Andrew Lavender of Pixalytics. Andrew had also been looking at the EU budget and wondering why Galileo was favoured over Copernicus?

Of course, as Hannes Dekeyser pointed out, there is a strategic dependence associated with Galileo that is not the same for Copernicus. Indeed, the whole Galileo programme was predicated on non-dependence – but this was at a time when there was no real global alternative to GPS. Glonass was incomplete Beidou was not even thought of. Interestingly, at that time, the UK government was opposed to the EU initiative on the basis of “GPS exists why do we need a second system?” This contrasts with the recent ambition to create the UK’s own Galileo once security signal from the EU one is to be denied them. The subsequent investment in Oneweb could be the subject of several more blog posts!

But we are interested in Copernicus and why this does not seem to leave the same impression with policy makers as Galileo. I content that this is because the general public are less aware of the benefits which satellite observations can bring. Just as the notorious US senator is quoted as saying “why do we need to invest in more weather satellites when I get thee weather every night on my television”, so the impacts of Copernicus are much more felt by businesses and by other government departments than by those taking spending decisions. Governments rely so much on focus groups to gather public opinion, and the general public is unaware. Whilst they have satnav in their cars and in their phones, there are very few EO applications which touch the citizens. Hence they remain unaware of the benefits and the public decision makers reflect their views.

Again, going back to Galileo. In the early days, when the debate over the programme was raging (this is 2001/2002), it was easy to engage a taxi driver in a discussion. What is this Galileo I keep hearing about on the radio? It is a European GPS. Oh well then it is a good idea. But, asked if they know of GMES (or Copernicus), there is no similar answer.

The conclusion is that we need to do much more to raise awareness of the impact EO and Copernicus has on everyone’s lives. Climate change gives us a good angle but our SeBS studies provide plenty more ammunition. I like Steven Krekels proposal concerning natural capital accounting. With so m much more awareness around environmental impact arising from the Covid pandemic, it is a good time to be raising awareness of the essential role played by satellites. The new CO2 monitoring mission will help grab attention but we cannot wait and need to promote the impact our technology has on everyday lives. It is true as Bert Rijk says that we have been going at this for 50 years, but this has been 50 years of science. Only now is the technology becoming mature to make a strong impact. Again, many of our SeBS cases show this very well. See the recent one on Norway where the benefit of the use of InSAR to help manage roads, rockslides and many other problems faced by Norwegian society is so clear – yet is only just starting to be appreciated. This is the same in many other countries and for many other issues of national interest.

I am sure we can develop a strong campaign. It is a personal target to contribute to this debate and to help develop both content and communications to deliver the messages. We are encouraging a community of interest called GeoValue with this particular goal and I look forward to working on this with yourselves and others on behalf of the sector.